We dive deep into why SSD prices are skyrocketing, and why we think they'll get worse in the near-term

The Highlights

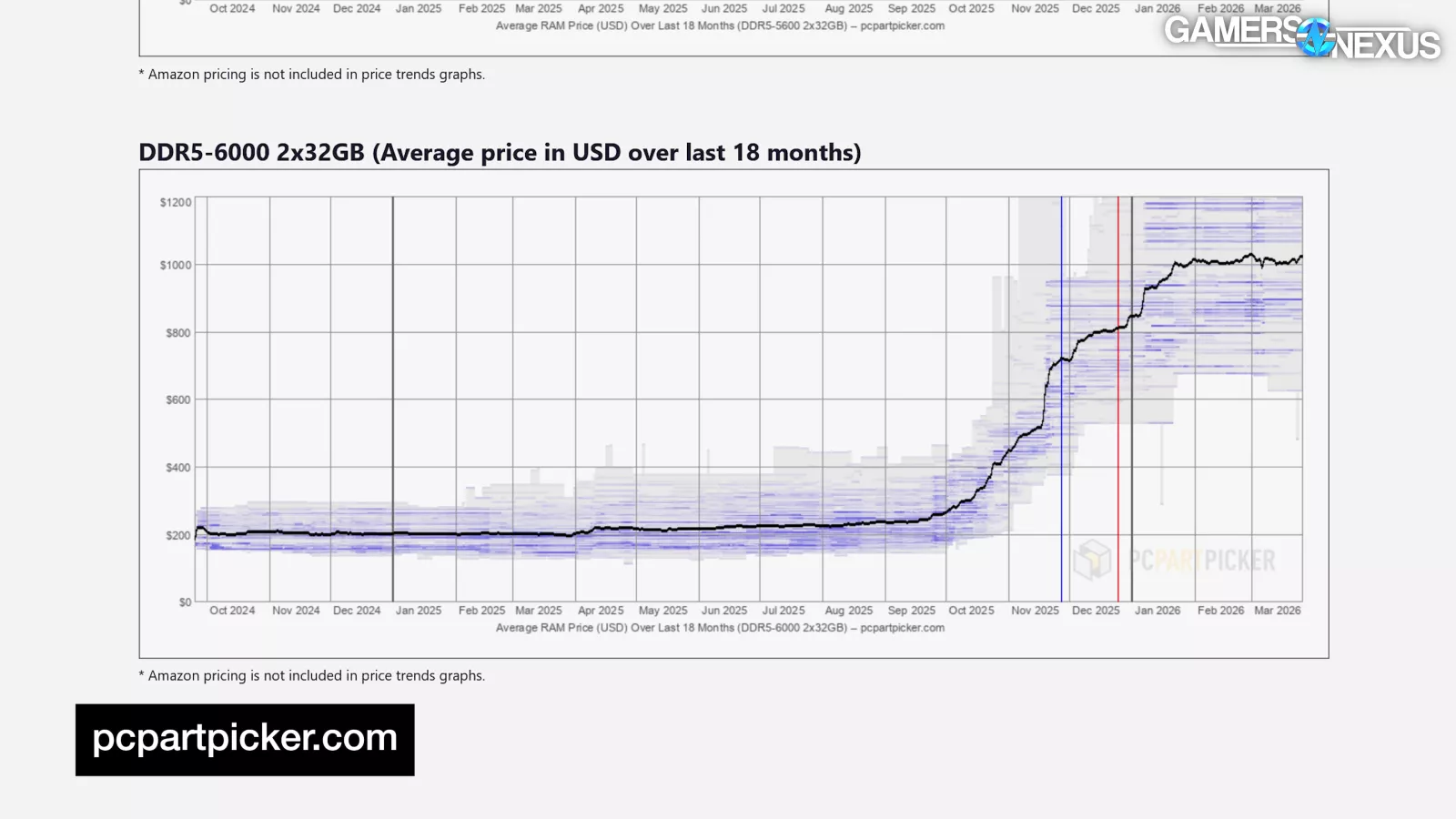

- Similar to RAM (DRAM) prices for system memory, SSDs are now plotting an actually worse price increase trajectory by time vs spot price, and we expect contract prices will trail

- Currently, data centers and "AI" are driving the demand for SSDs to be deployed in server solutions worldwide, which reduces consumer demand

- Some SSD NAND suppliers are reducing their production capacity despite high demand

Table of Contents

- AutoTOC

Intro

The manufacturers and AI data centers responsible for the ongoing RAM and GPU shortages and price surges that we’ve previously covered have decided it was finally time to do the same exact thing to SSDs with a more latent impact to consumers.

Editor's note: This was originally published on March 28, 2026 as a video. This content has been adapted to written format for this article and is unchanged from the original publication.

Credits

Host, Writing

Steve Burke

Video Editing

Vitalii Makhnovets

Tim Phetdara

Writing

Tannen Williams

Writing, Web Editing

Jimmy Thang

In the data we compiled from multiple sources, NAND spot prices in some instances -- like 512Gb TLC -- increased by nearly 9x in a span of 6 months.

That hasn’t fully hit completed consumer device prices yet, but it’s starting to.

Prices are skyrocketing due to a combination of a few things.

Partly thanks to data centers, there’s now a hard drive shortage, alongside unforeseen data center Flash storage demand, manufacturers prioritizing production of higher-margin enterprise SSDs, and some manufacturers intentionally cutting output amidst the increasing SSD shortage in order to protect their profitability, effectively drying up supply of consumer SSDs.

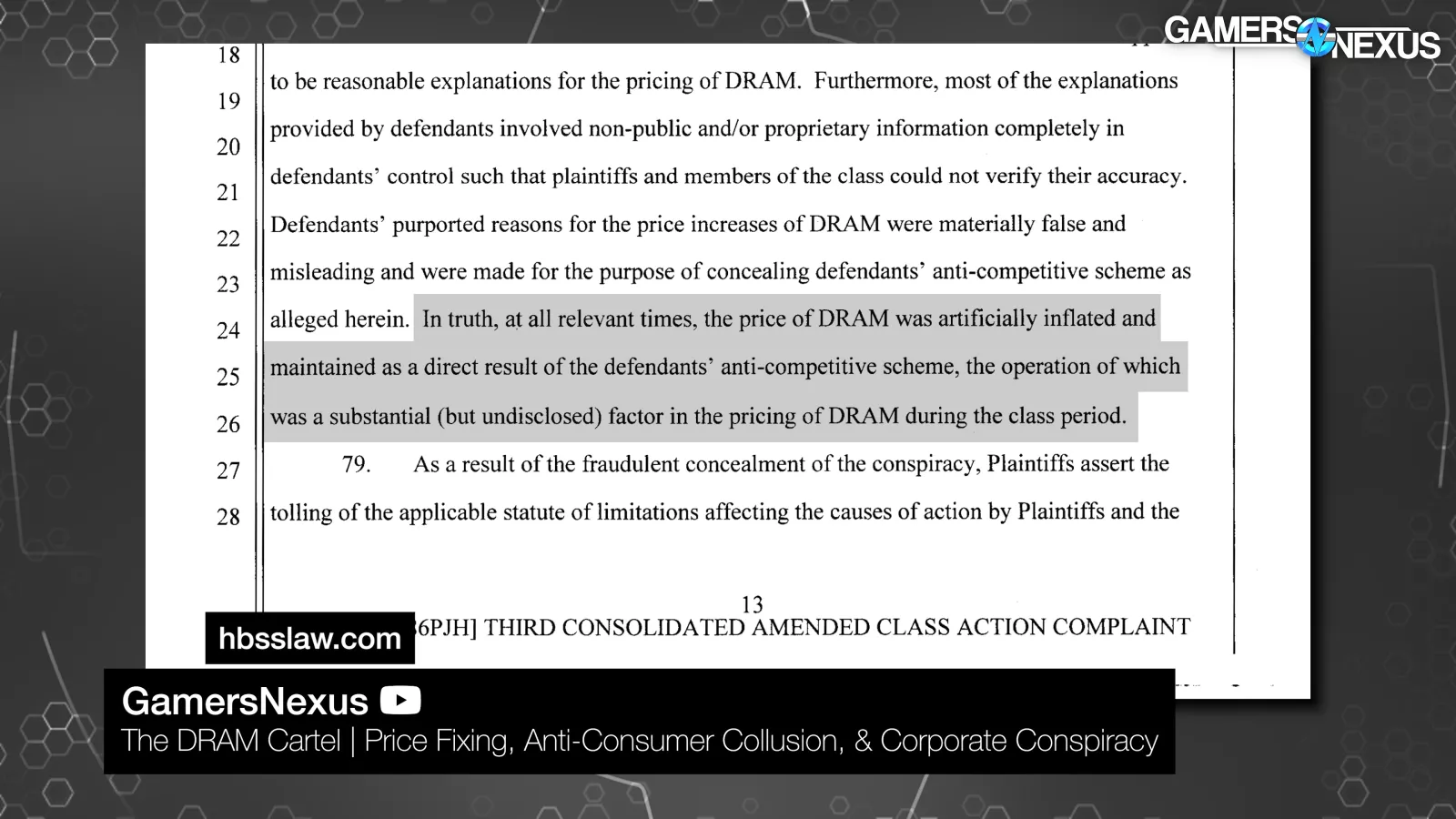

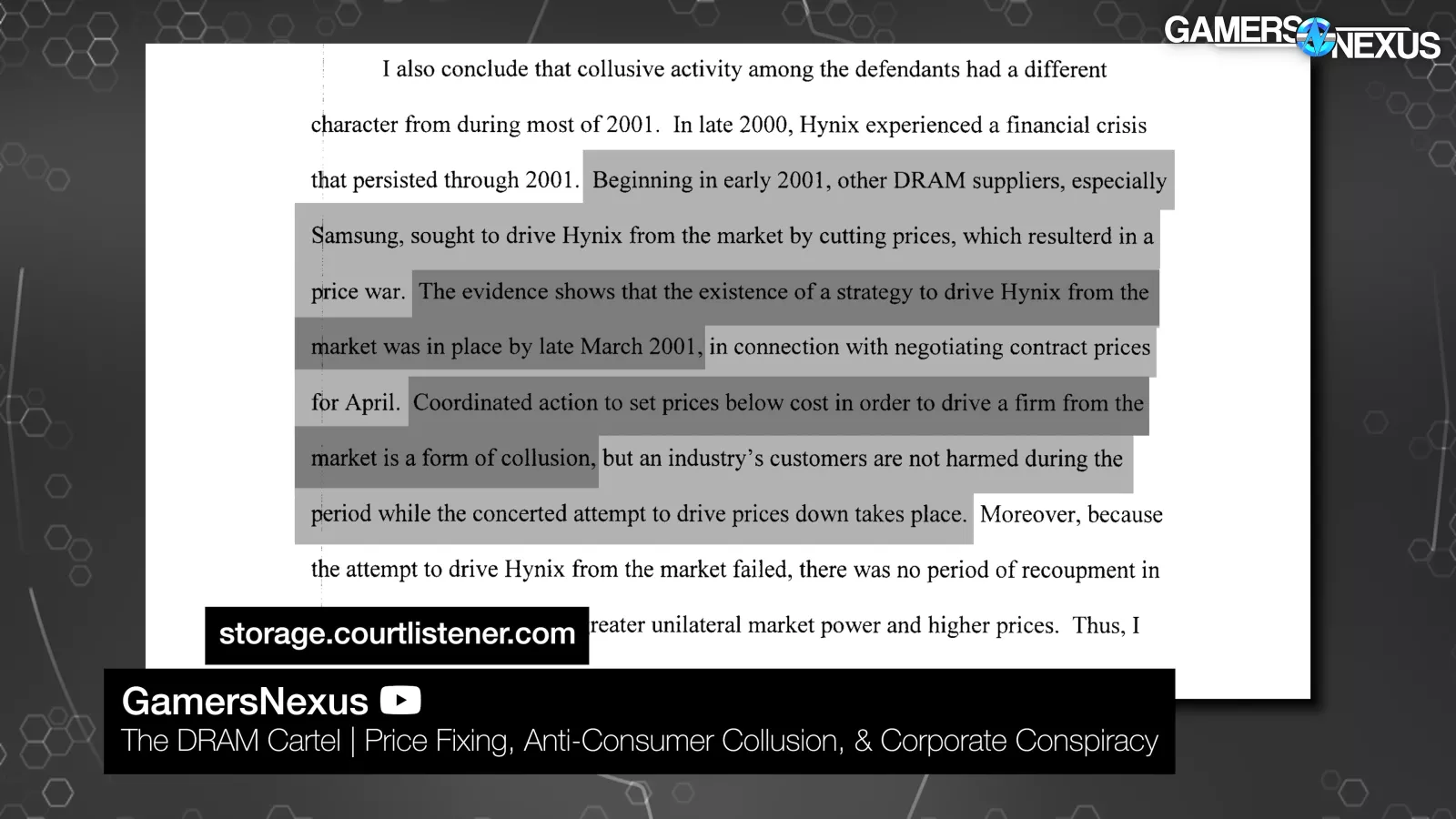

If that sounds familiar to the DRAM cartel history piece we ran, it should: It’s the same companies playing the same games, where they know demand is up and they’ve openly stated that they’re prioritizing protecting their profit rather than meeting demand -- and this happened just as Chinese NAND maker YMTC came online in a larger way, which keeps the incumbent margins up.

Since October, the session AVG for 512Gb (Gigabit) TLC supply increased from $2.70 to over $23, or by more than 8.5x its previously stable spot price, even surpassing DDR5 16Gb’s recent spot price surges in terms of percent increase.

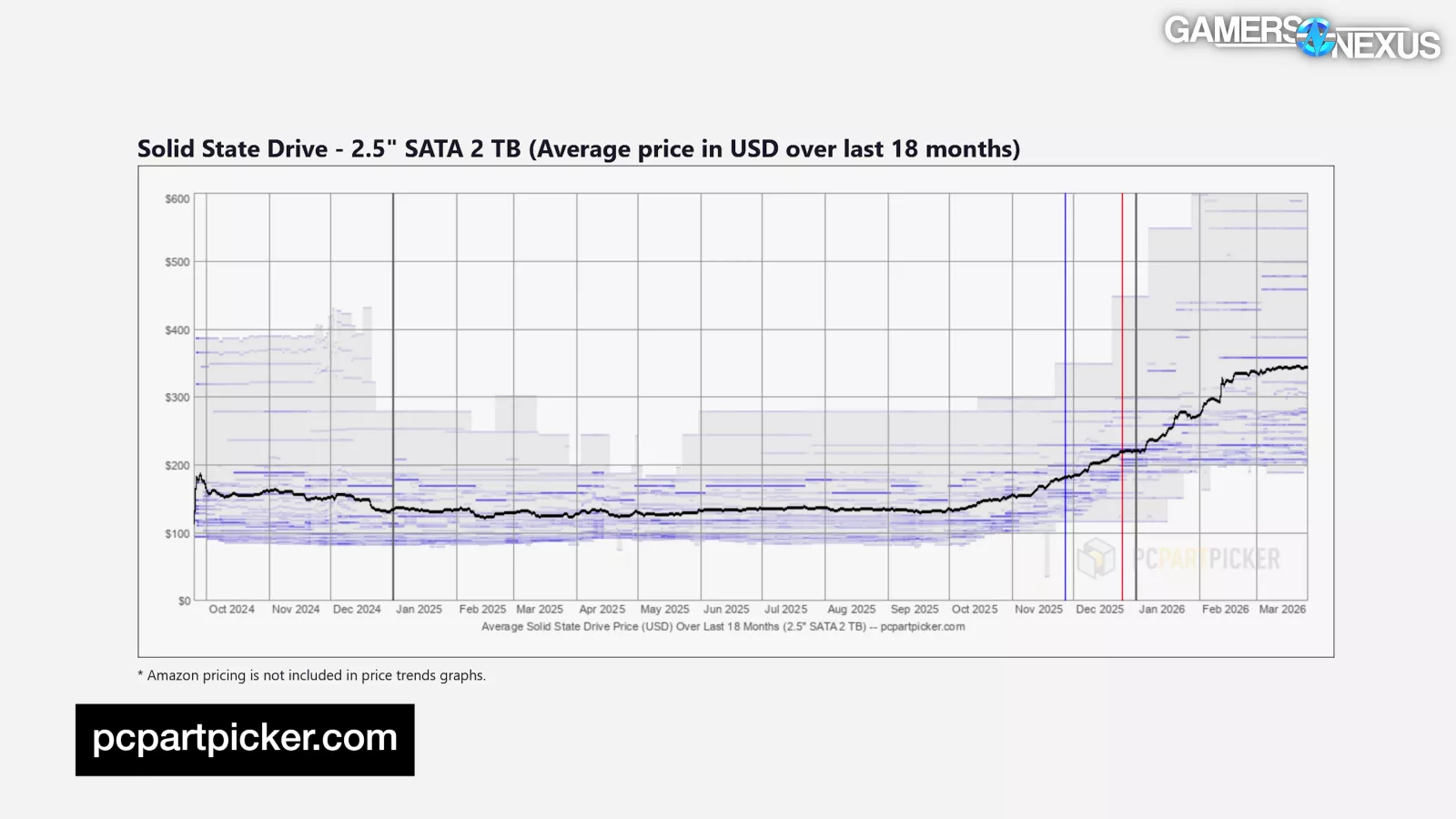

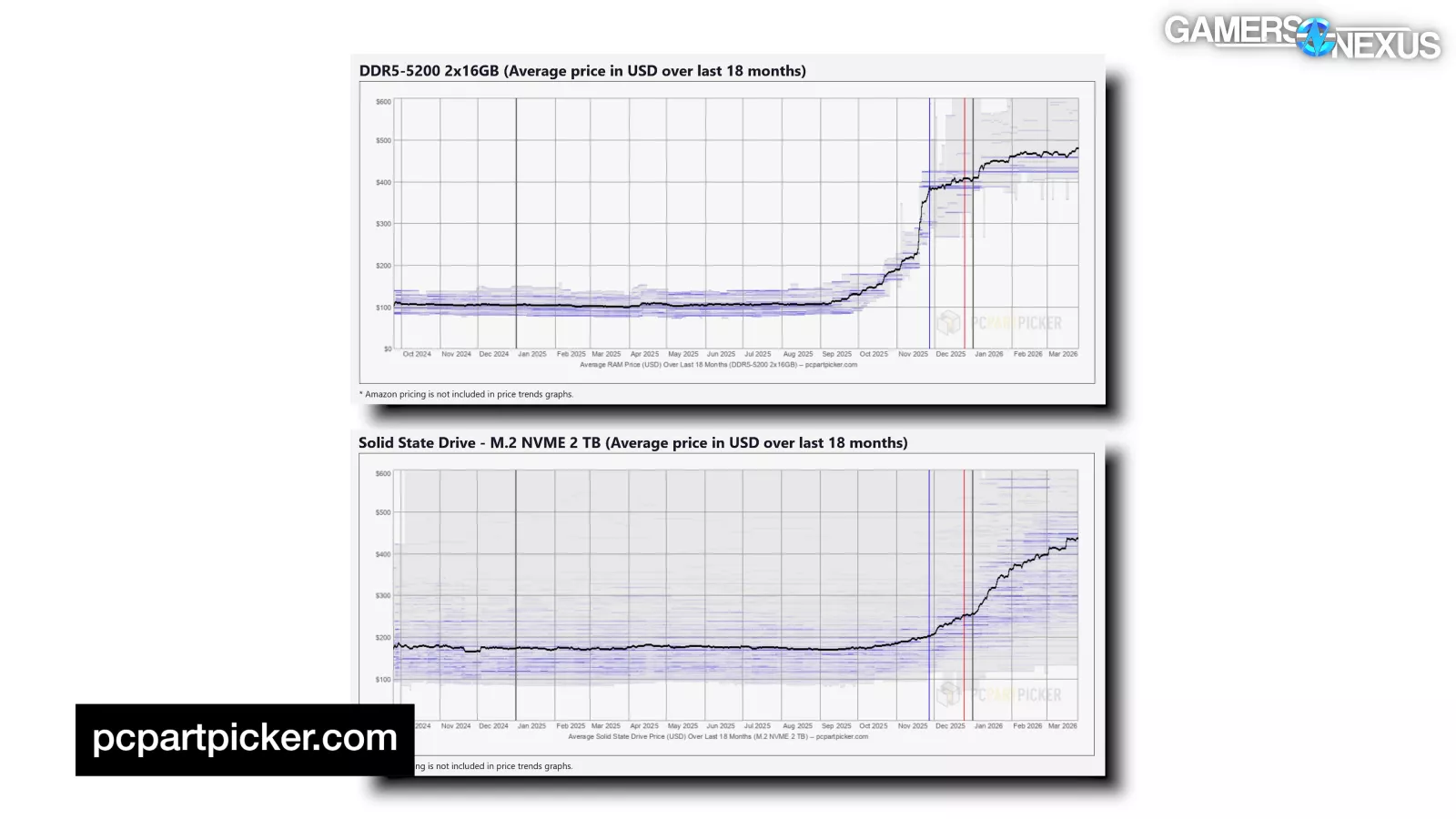

The AVG 2TB SATA SSD’s price increased from around $150 in November to $350 currently, while the AVG 2TB NVMe SSD soared from around $190 to nearly $450, at the time of writing for consumers.

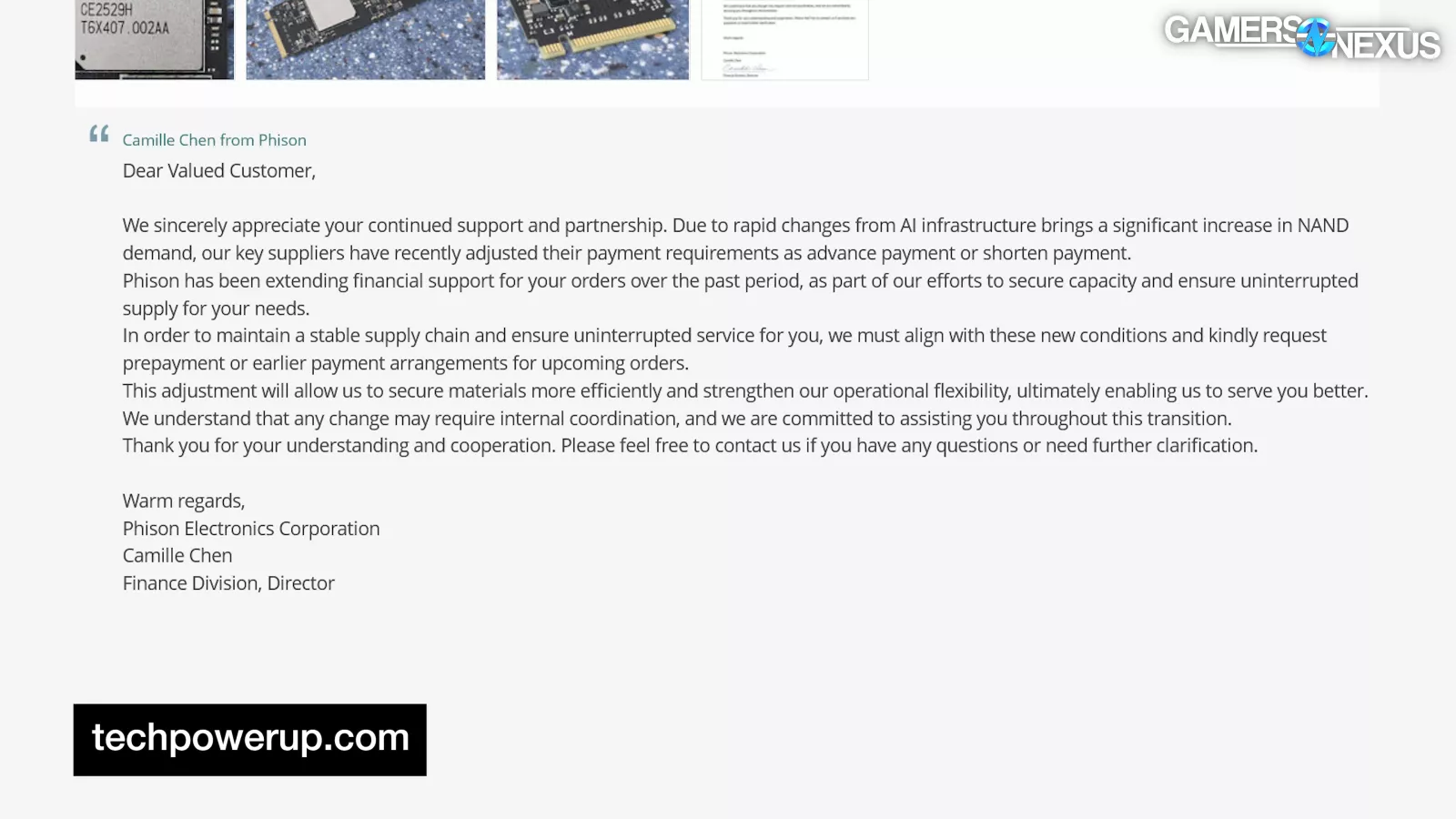

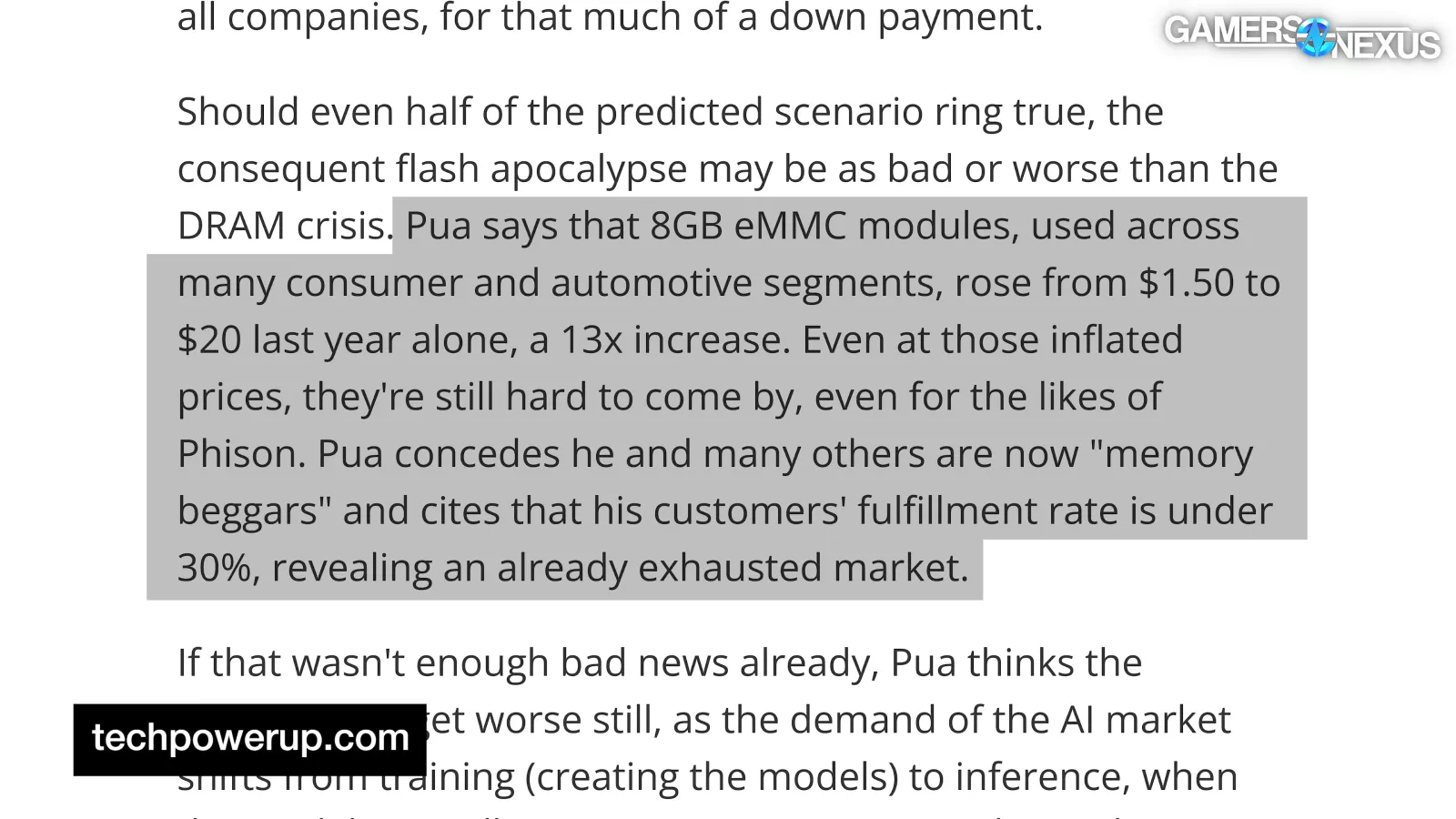

Phison, a NAND controller manufacturer, has reportedly begun requesting prepayments on orders. The CEO claims that 8GB eMMC, or embedded multi-media card, modules “rose from $1.50 to $20 last year alone,” and notes an under 30% fulfillment rate, as reported by Tom’s Hardware.

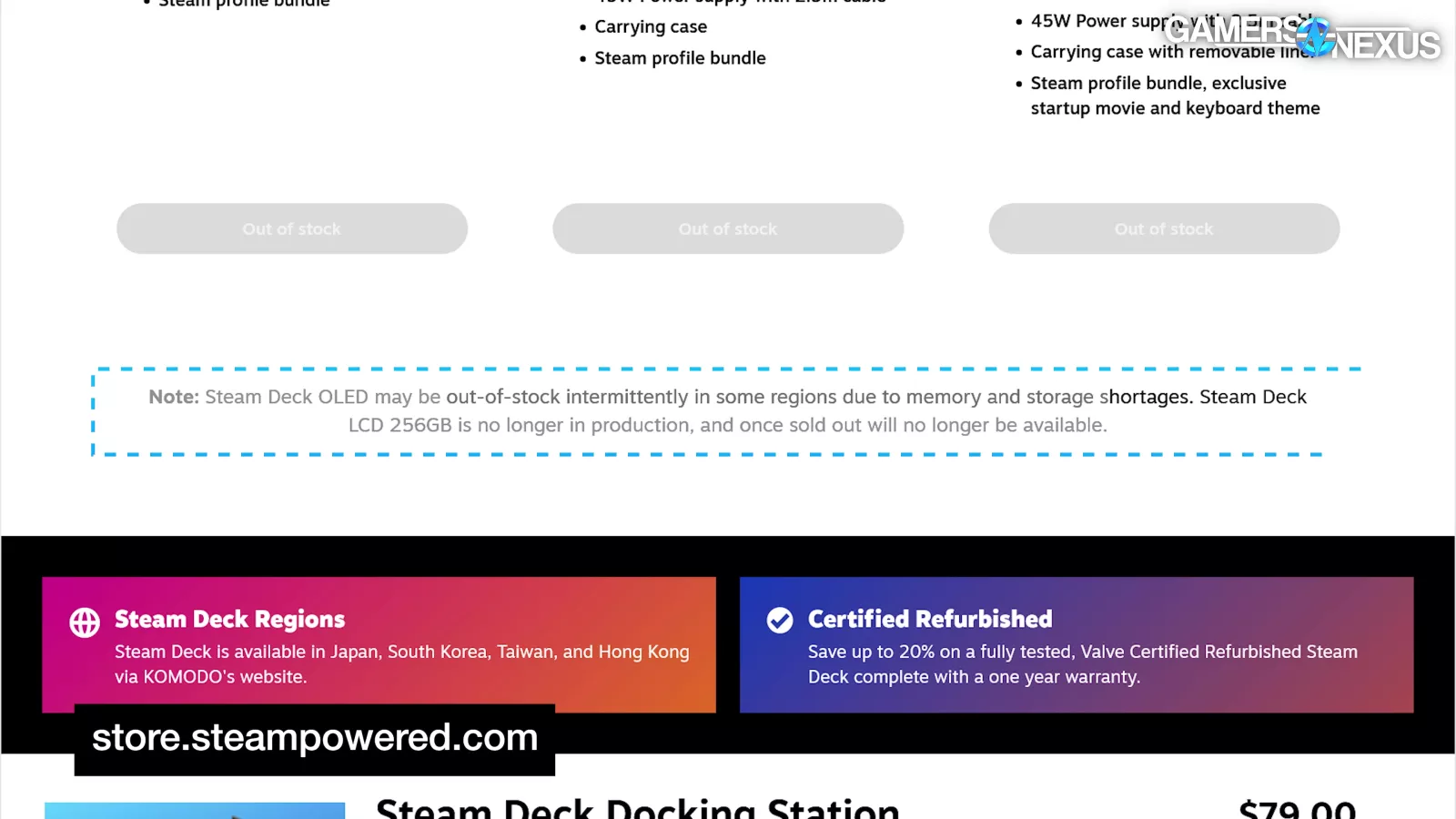

Valve says its Steam Deck is out of stock “due to memory and storage shortages” and previously cited issues with Steam Machine and Steam Frame pricing due to memory and storage.

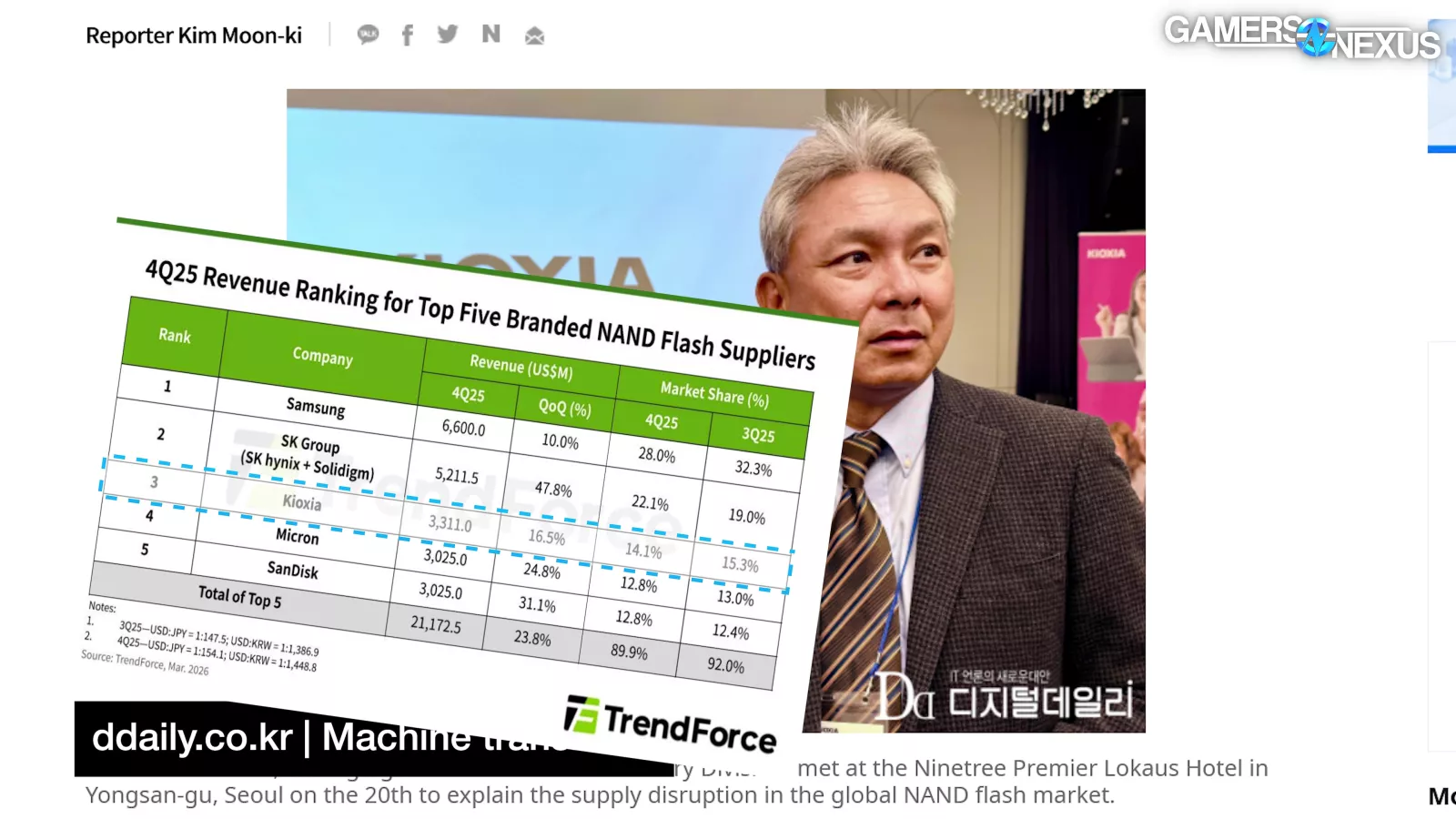

A managing director for Kioxia, the 3rd largest NAND manufacturer with over 14% market share, told Digital Daily (through machine translation): “To be honest, this year’s production is already ‘sold-out.’”

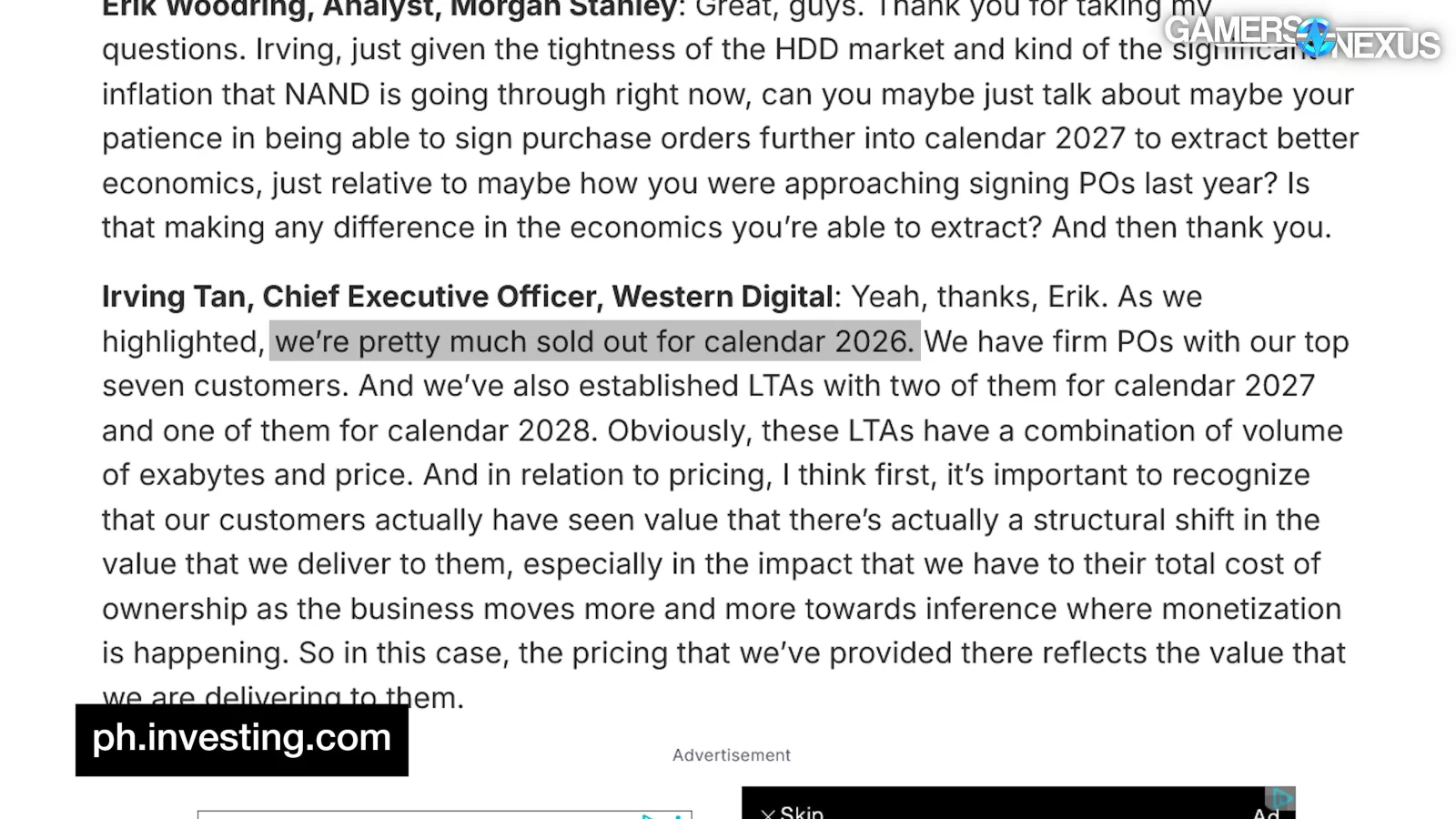

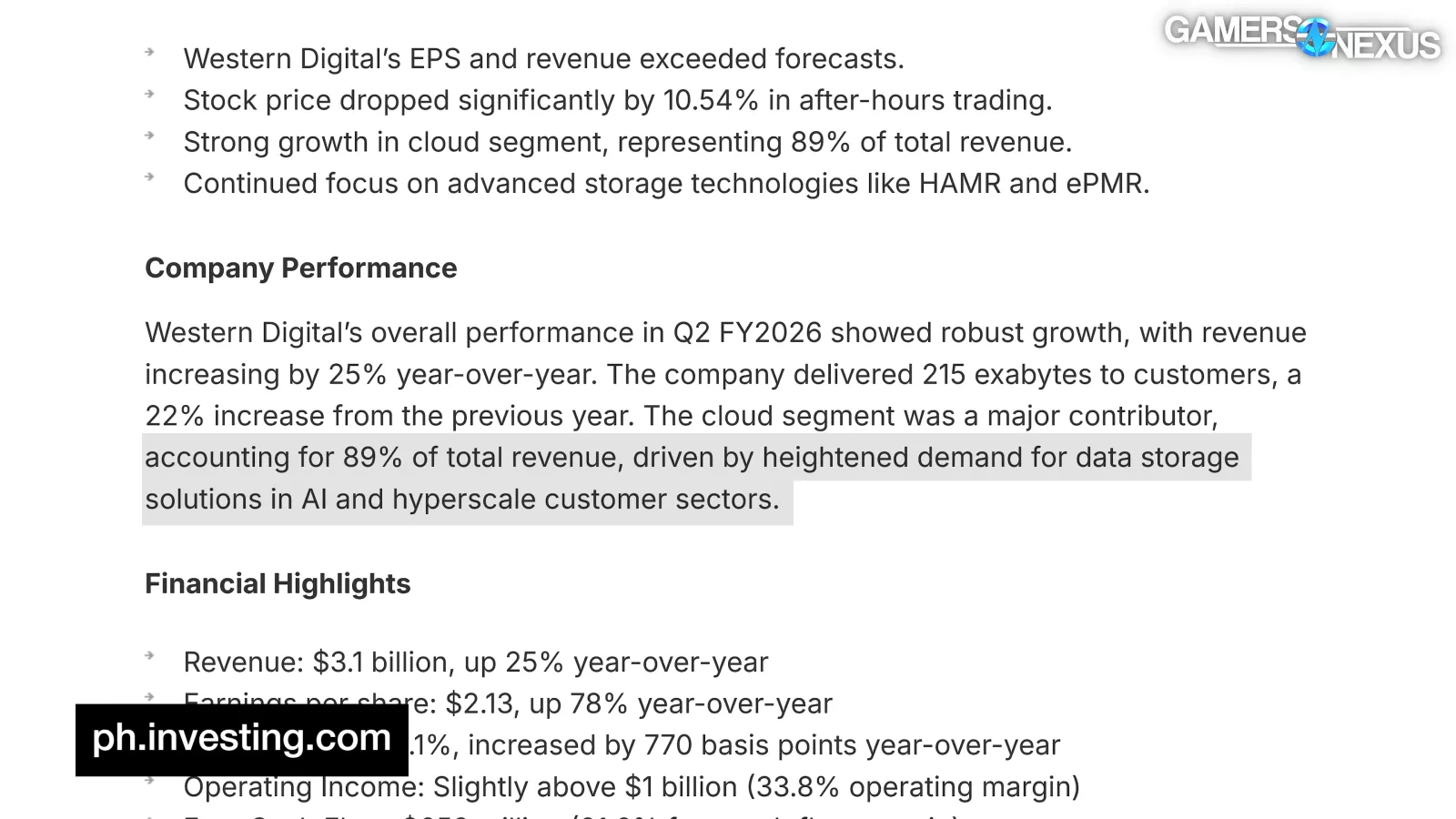

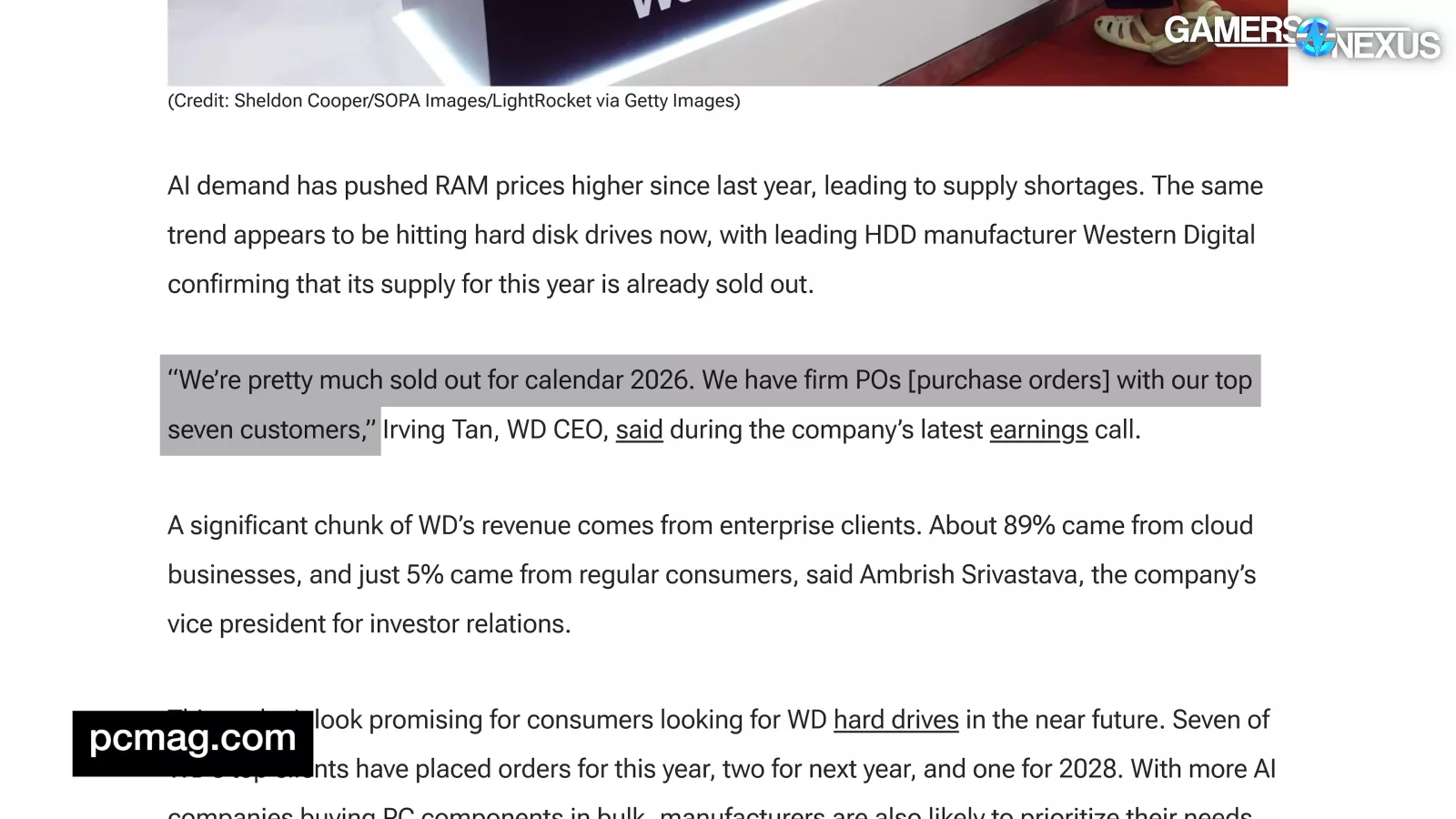

Similarly, the CEO of Western Digital, the largest hard drive manufacturer, disclosed in its Q2 ‘26 earnings: “We’re pretty much sold out for calendar 2026,” attributing 89% of its second quarter revenue to its cloud segment.

Meanwhile, some manufacturers are reportedly purposefully constraining supply amidst the shortage and prioritizing higher-margin enterprise SSDs over consumer SSDs.

ChosunBiz, citing Omdia, reports: “Samsung Electronics slightly lowered its NAND wafer output from 4.9 million last year to 4.68 million this year. [...] SK hynix's NAND output is also expected to follow a similar path, from around 1.9 million last year to 1.7 million this year.”

Reported via Yahoo Finance, Citi estimates that “NAND demand driven by ICMS,” or NVIDIA’s Inference Context Memory Storage platform, is projected to represent “2.8% of expected global NAND demand in 2026 and 9.3% in 2027,” meaning that NVIDIA will more than triple the storage needs of this specific solution against global NAND demand.

And TrendForce adds:

“The surge in NAND Flash demand is structural, not temporary. This trend is fueled by the fast-growing needs for AI storage and HDD supply shortages, leading CSPs to reallocate orders to enterprise SSDs.”

Kingston’s Datacenter SSD Business Manager, noticing early market indicators, commented on the situation back in December, saying, “There has been a little bit of a delayed reaction, but I think come January, February, I think it’s going to be very well known across the board that SSD prices have significantly increased.”

Luckily, NVIDIA CEO Jensen Huang recently detailed precisely why we’re seeing these sudden price surges, explaining, “And so, I think the fact that everything is scarce is fantastic for us.”

That’s right. Everything being scarce is fantastic for not just NVIDIA, but the suppliers of Flash and DRAM.

Overview

SSD price increases are from NAND Flash undergoing an identical situation to DRAM, which we detailed in our “RAM: WTF?” video on the channel.

We’ll kick off with a quick look at NAND supply spot prices, including how it relates to both DDR4 and DDR5 spot prices. Then, we’ll review individual SSD prices, also examining how SSDs using Chinese manufacturer YMTC’s NAND Flash compare in price, before discussing the mixture of factors contributing to this mayhem in more depth.

Some basics first:

The NAND Flash Industry

In contrast to DRAM, which is volatile storage, NAND Flash is non-volatile. The difference is that volatile storage loses retained information with power loss, whereas non-volatile storage persists without a power source for an extended period of time.

Despite their different uses, there are several parallels between the DRAM and NAND industries.

First, both are largely controlled by the same manufacturers.

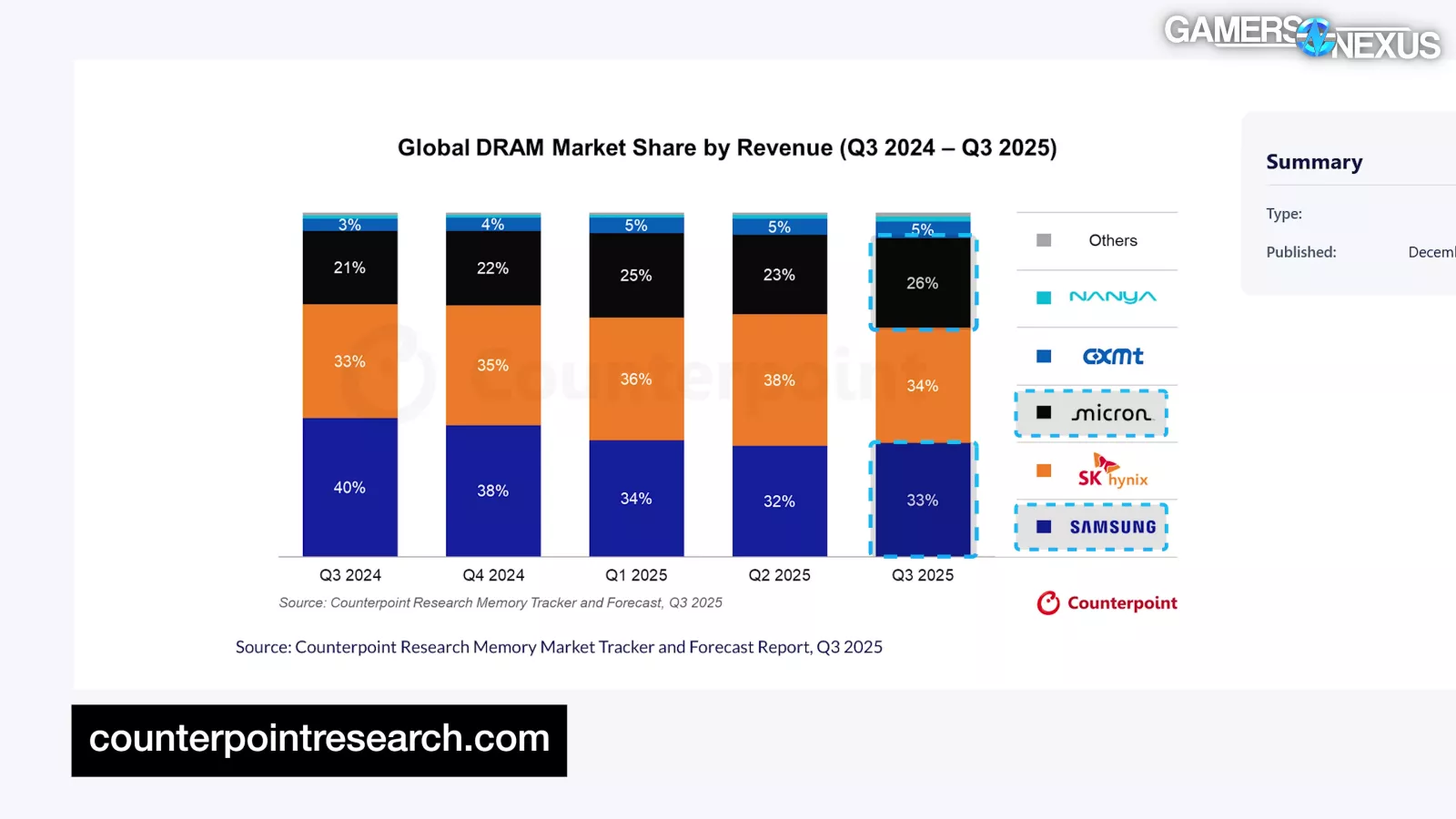

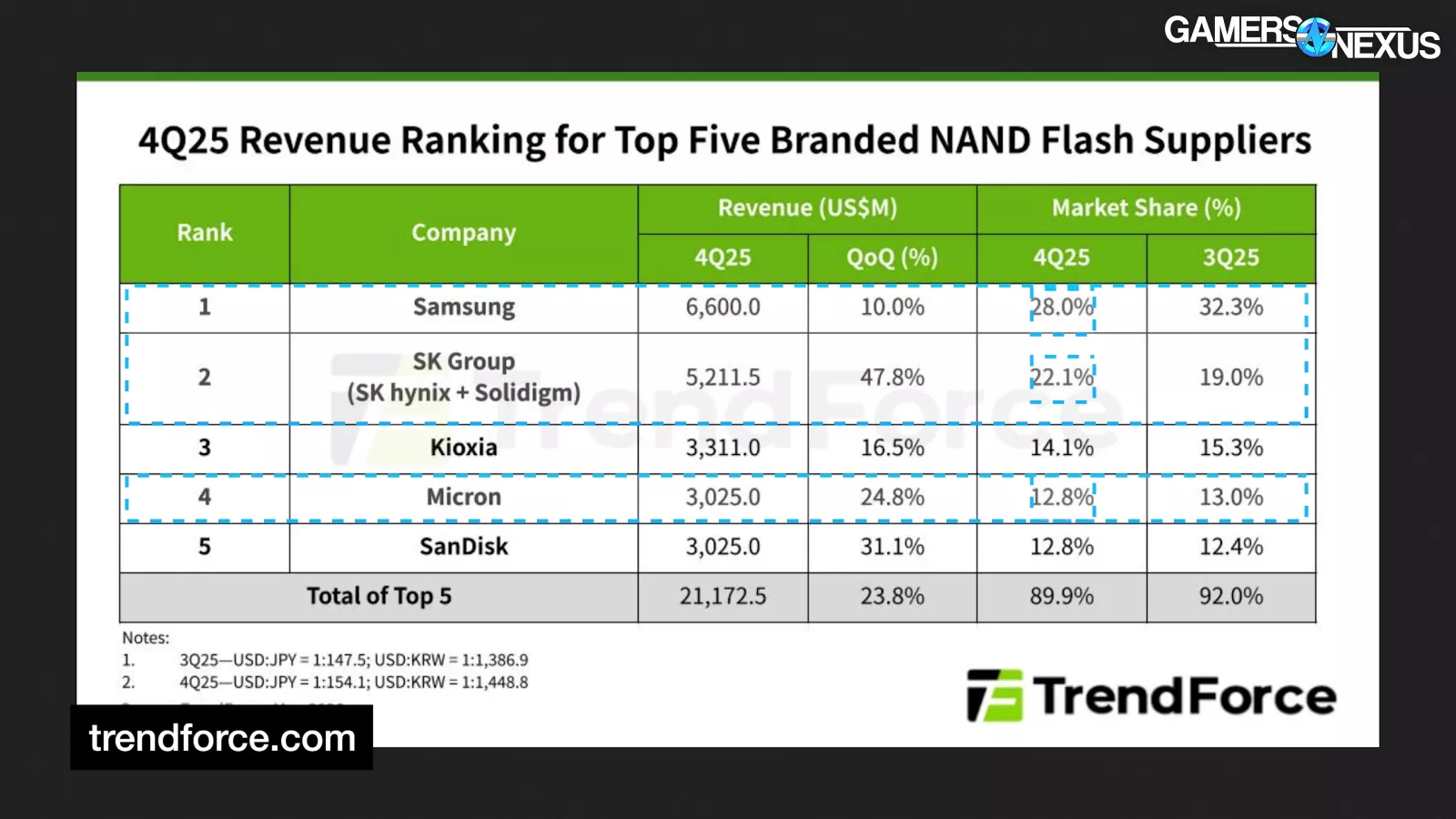

Samsung, Micron, and SK Hynix, who control a collective 93% of the DRAM market, also hold a combined 62.9% of the NAND Flash market, with Kioxia (formerly Toshiba Memory), SanDisk, and Chinese newcomer YMTC making up the remaining 37% share, according to TrendForce and Counterpoint Research’s most recent publicly available market share by revenue data.

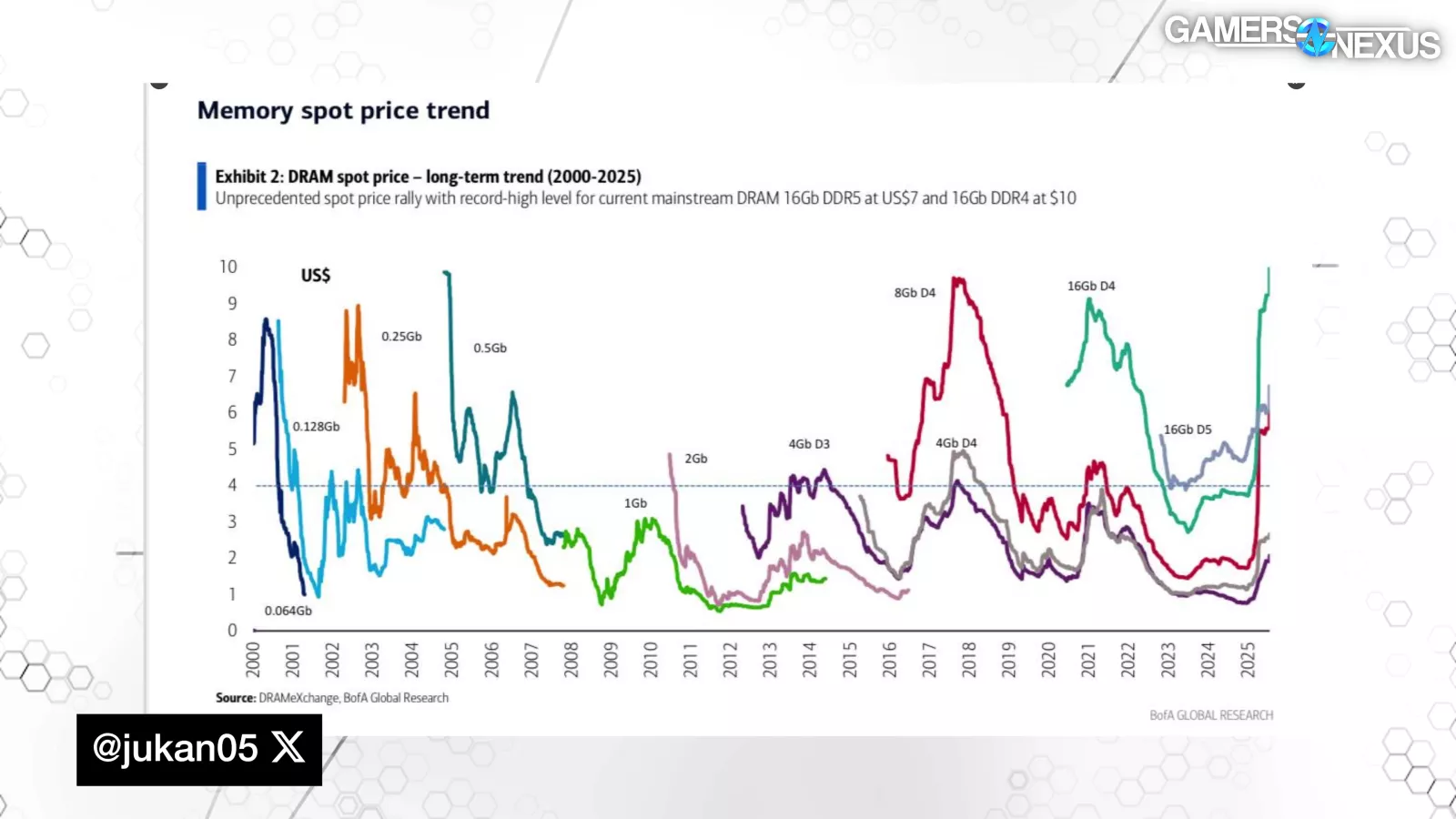

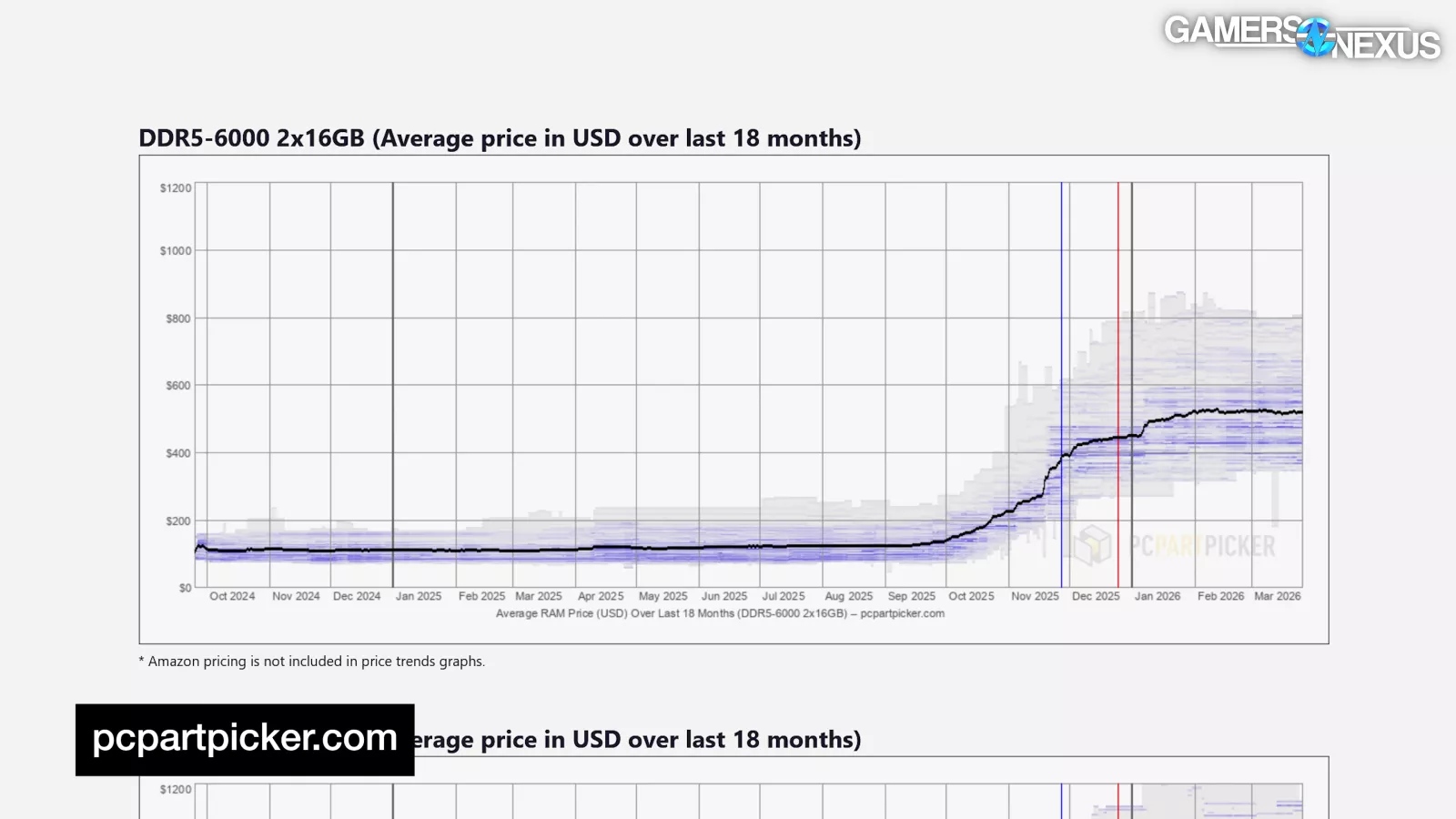

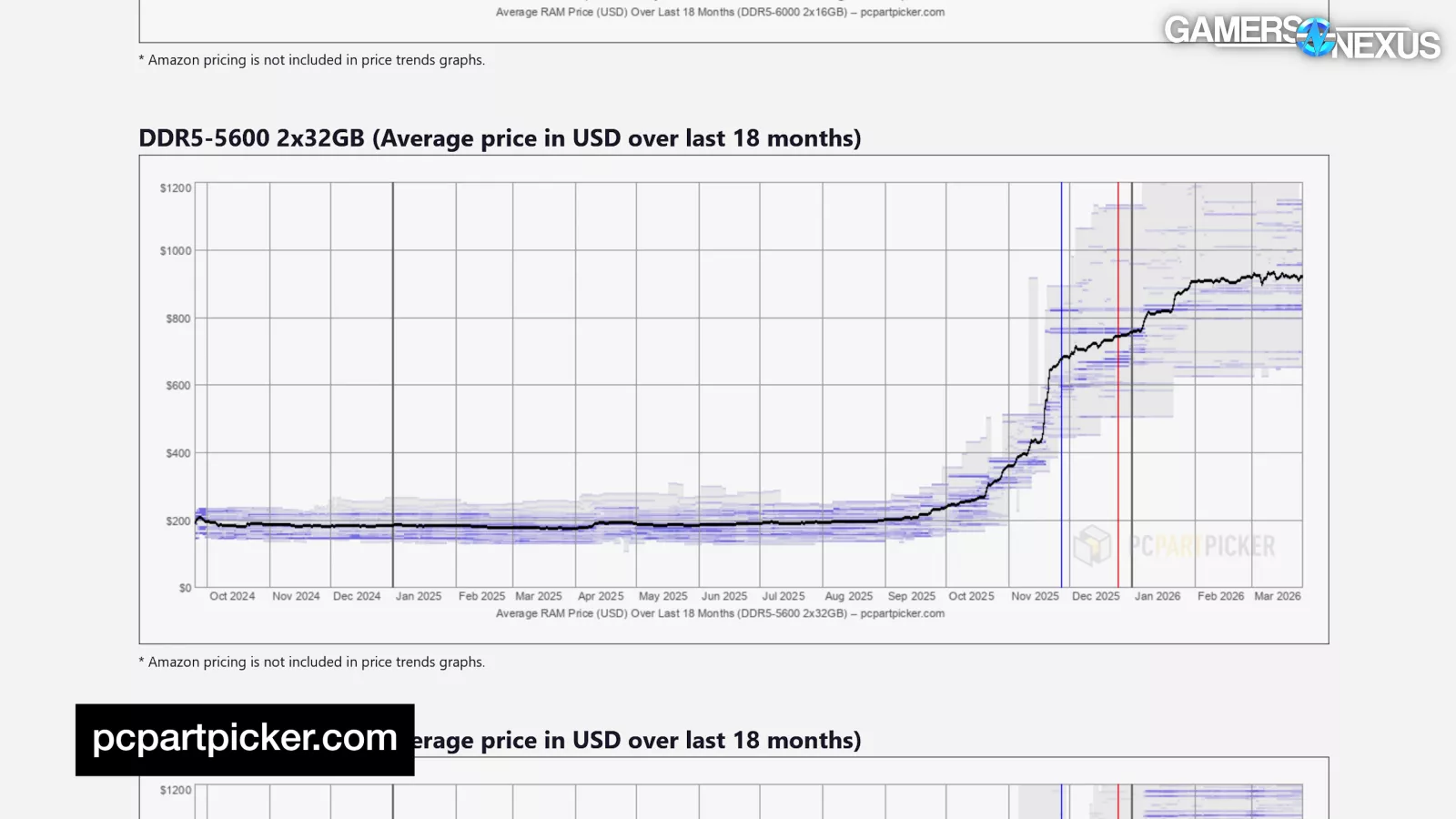

Another characteristic that both markets share is their pricing typically following a cyclical pattern, meaning prices for each new DRAM or NAND generation usually peak early in the product lifetime and gradually decrease over time, as seen in the above long term trend of DRAM spot prices, shared via Jukan on Twitter.

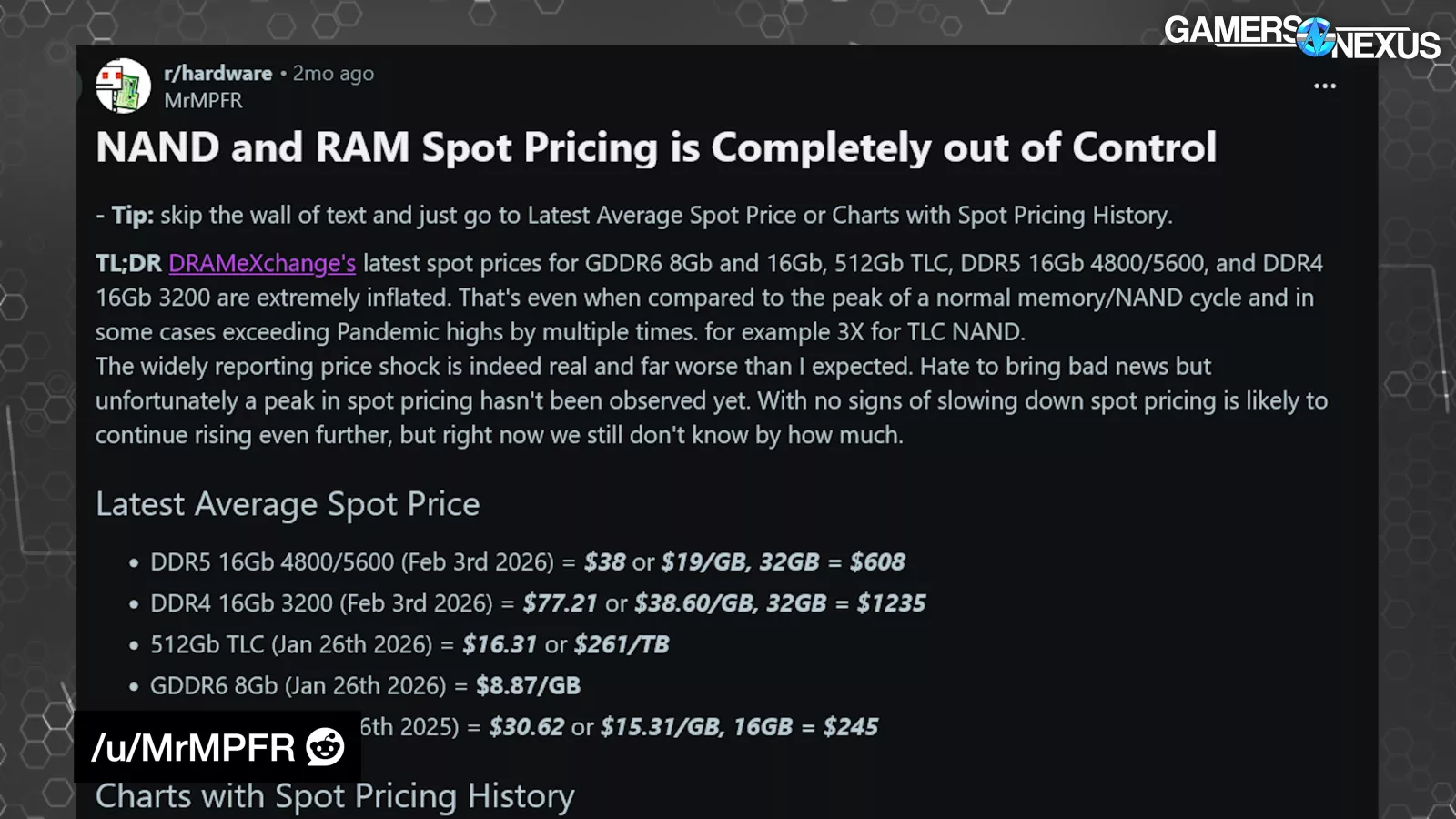

This current demand influx is generating abnormal price spikes regardless of the product’s lifetime, and prices are consistently increasing as opposed to the normal pattern of reducing over time, as seen in this 512Gb TLC Spot Price History chart shared by u/MrMPFR on Reddit, which compiles data from other sources like DRAM Exchange.

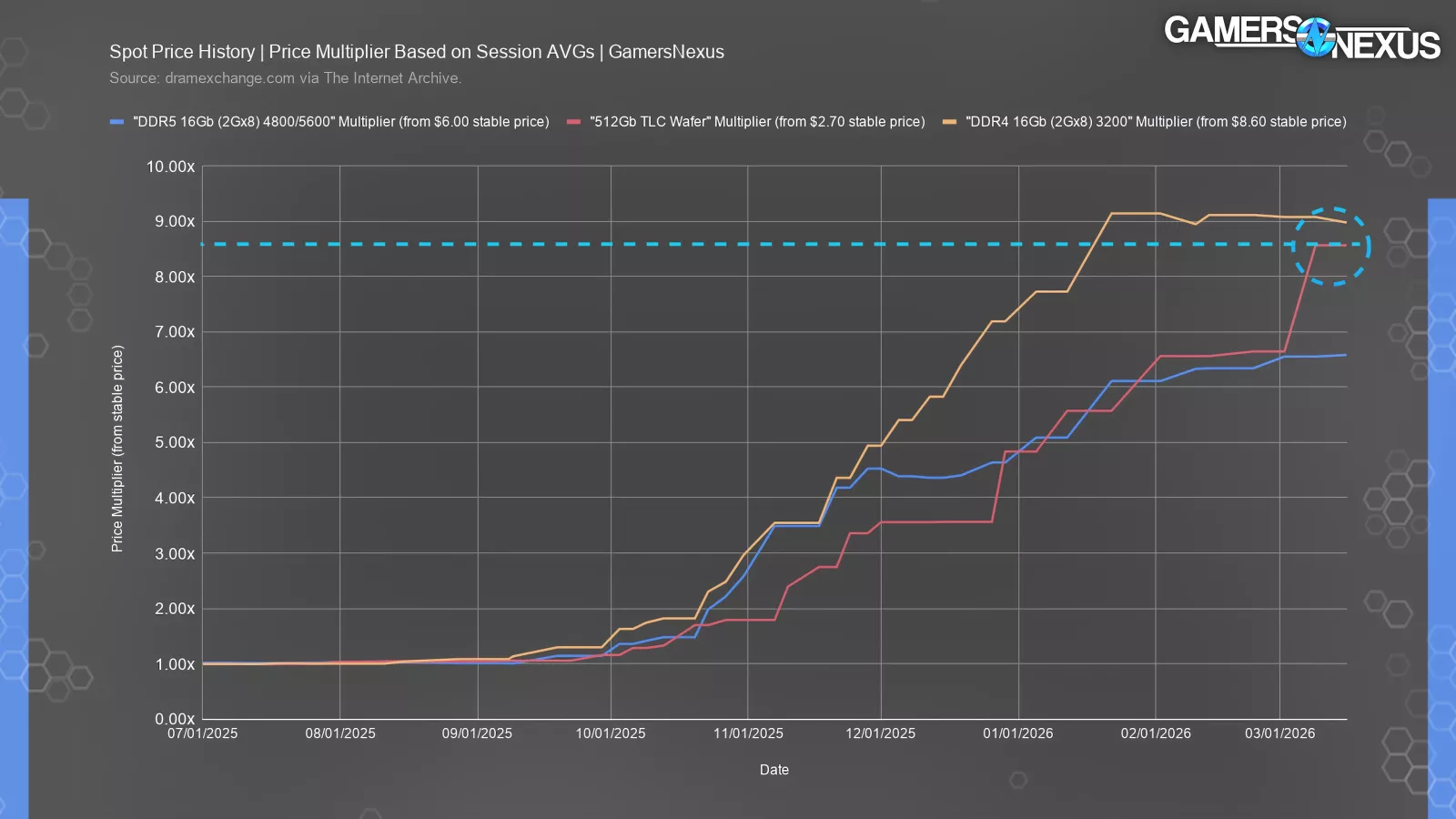

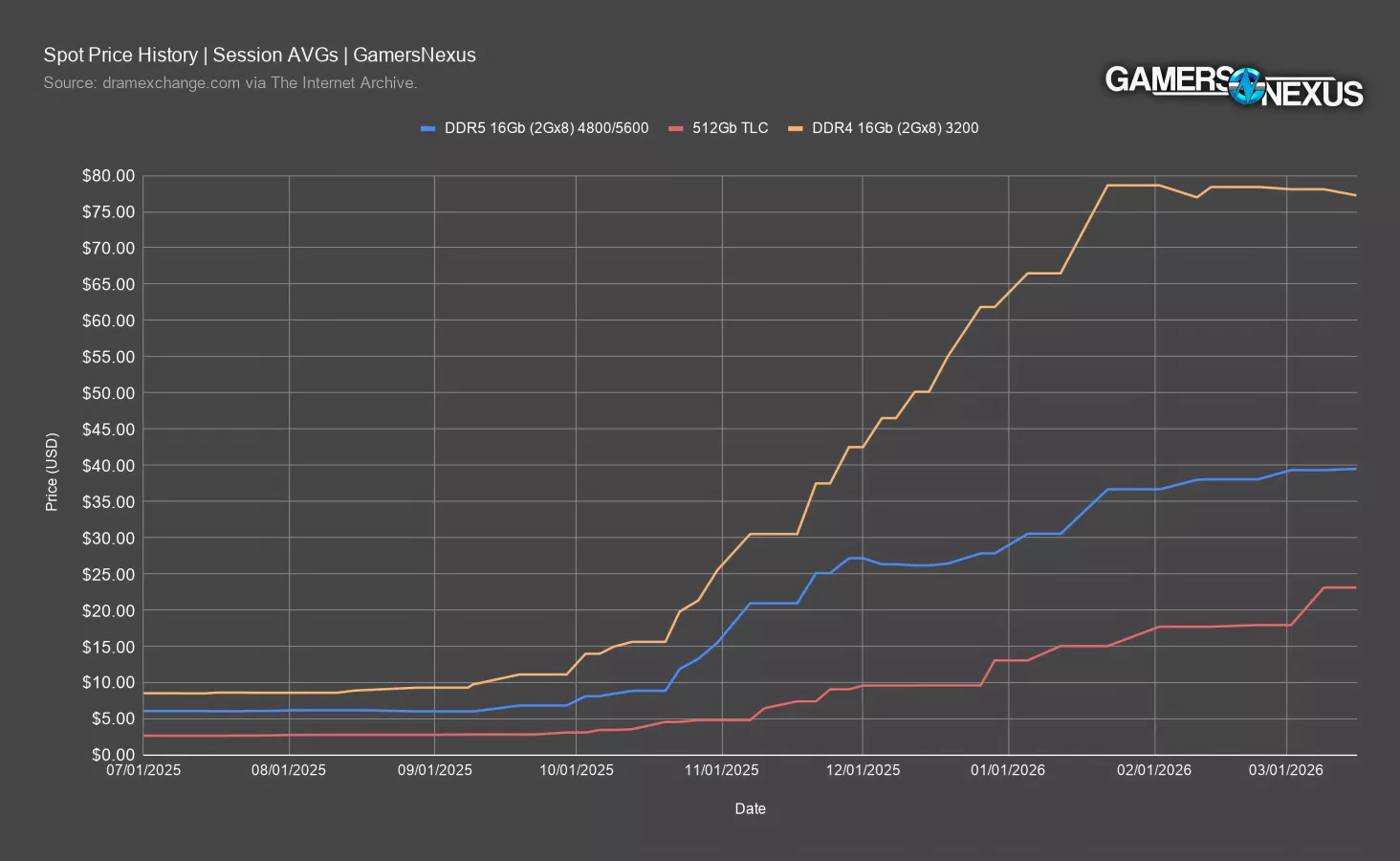

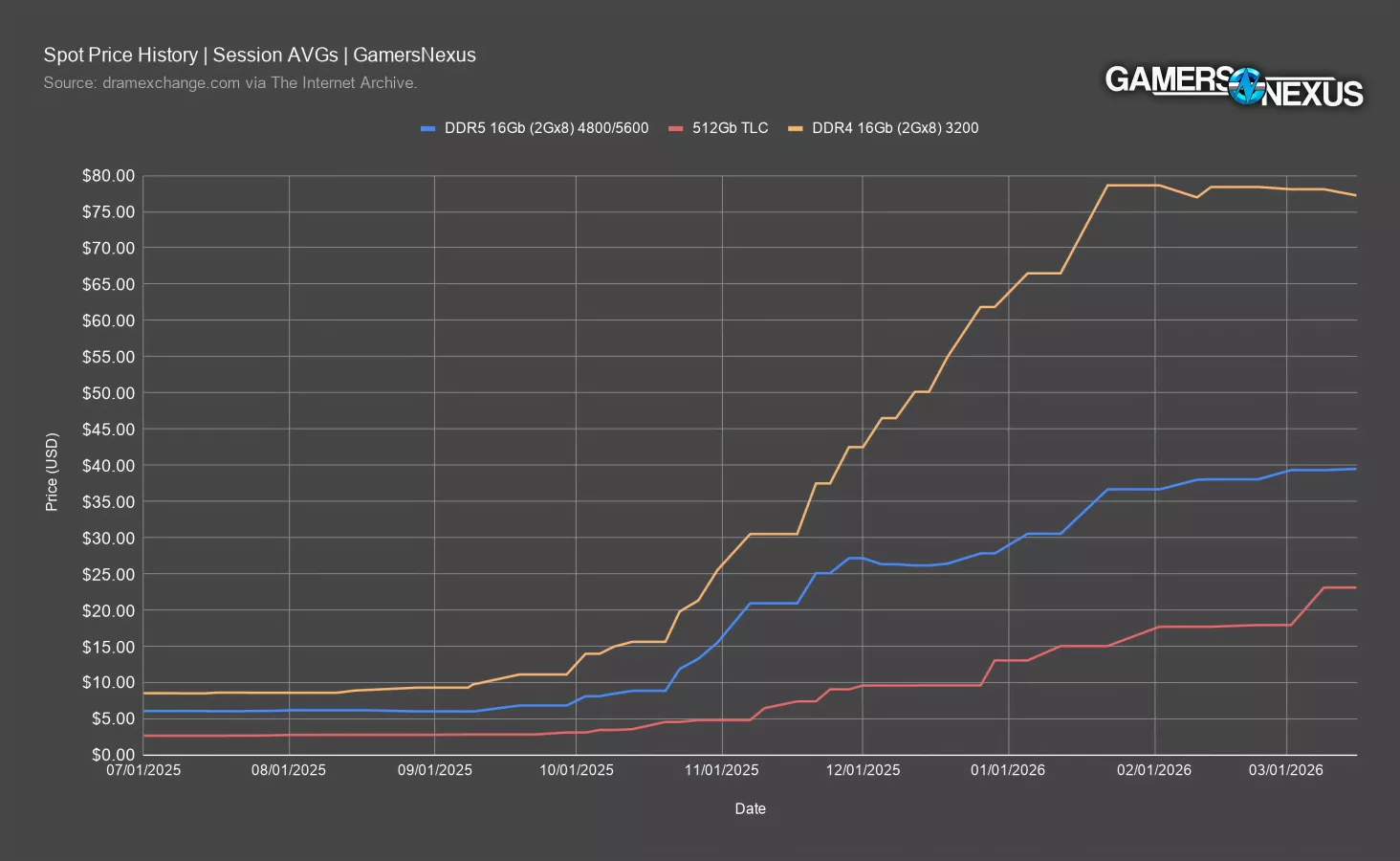

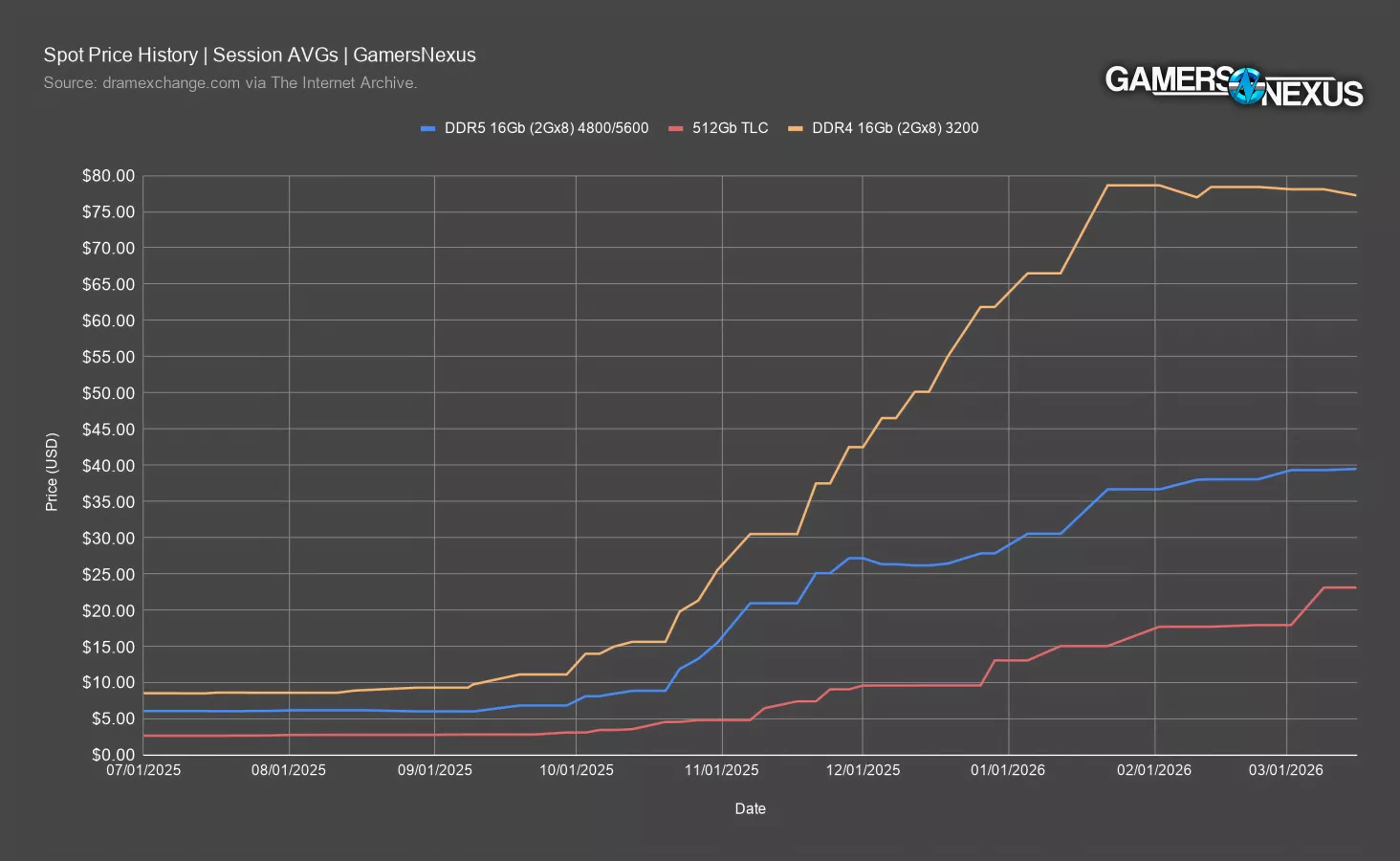

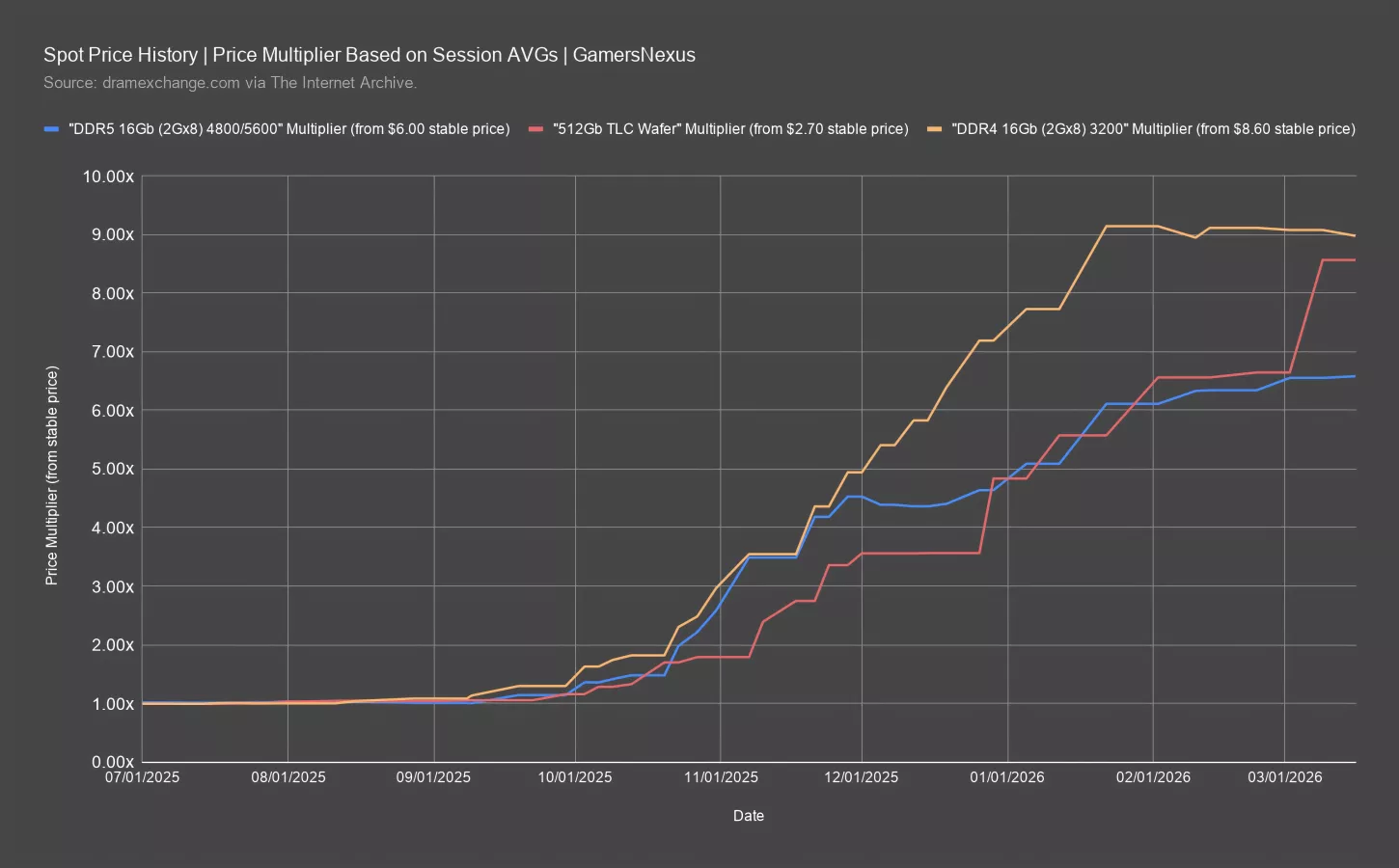

Spot Price History

This chart plots spot price session AVGs from July 2025 to March 2026 for DDR5 16Gb, 512Gb TLC, and DDR4 16Gb. We collected this data using the Internet Archive to compile a brief spot price history as updated on dramexchange.com. These are supply costs. Contract prices are often different, but spot prices give us an idea for upstream supply chain pricing.

DDR5 16Gb’s session AVG skyrocketed from under $10 in October to over $25 by the end of November. Then, it exceeded $30 in early January and surpassed $35 heading into February, and is now approaching $40 spot. The spot price for DDR5 16Gb at lower speeds has gone up by at least 6-6.7x since late August last year.

As we already know, the end result is that a lot of the most common kits of memory have multiplied in price upwards of 5x or more in just as many months.

512Gb TLC (or triple-level cell) spot prices were around $2.50 to $3 until October. Since November, the 512Gb TLC session AVG has increased by around $5 or so monthly, up to its current $23 session AVG. That’s an increase of about 8.5-9.0x since September, worse than what we’re seeing with DDR5, actually, by a lot.

DDR4 16Gb’s session AVG experienced the greatest surge, seemingly disproportionately affected by EOL announcements causing low supply and surging stockpiling demand, soaring from about $8 in August, to $15 in mid-October, to nearly $80 by mid January, where it’s remained since.

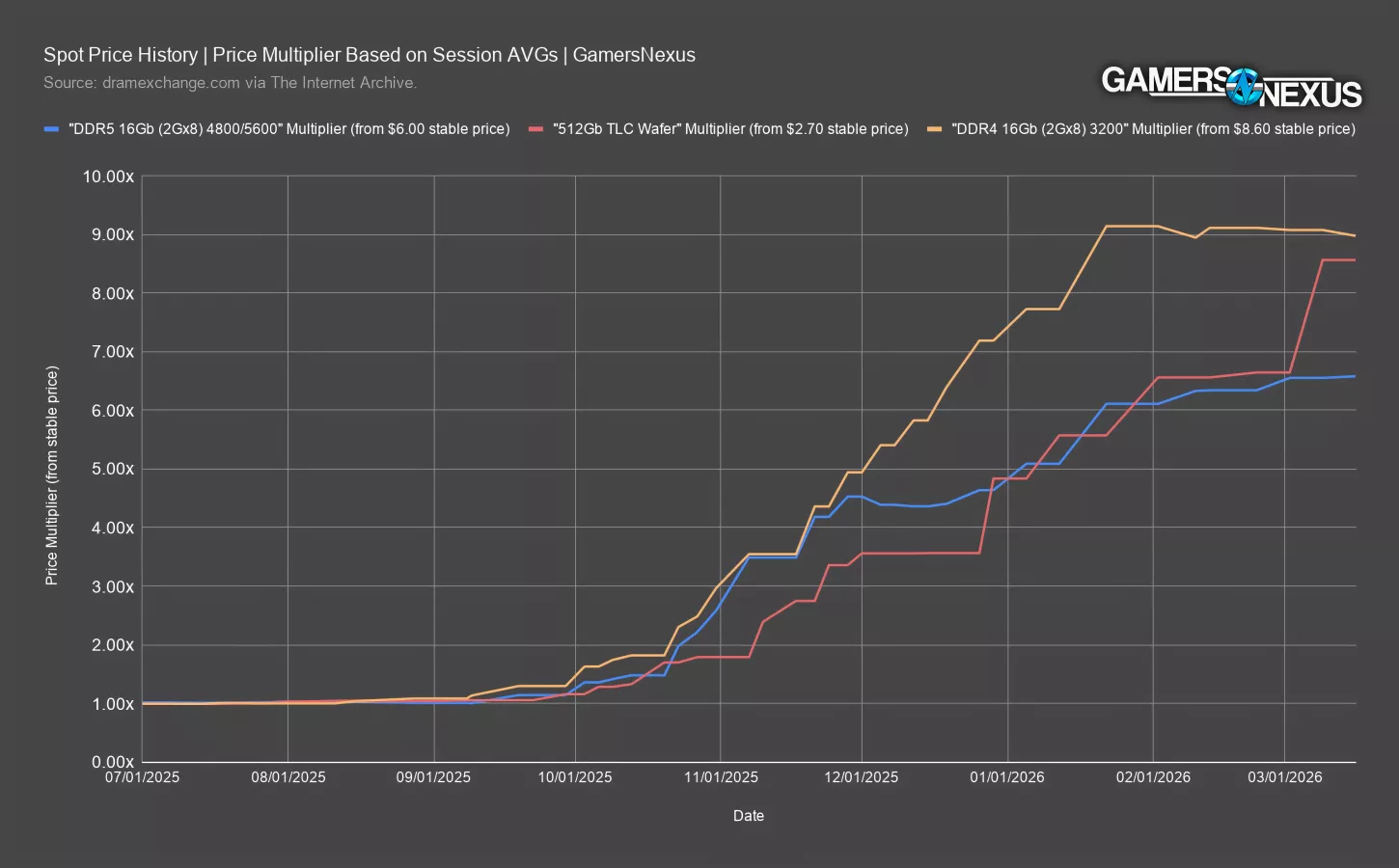

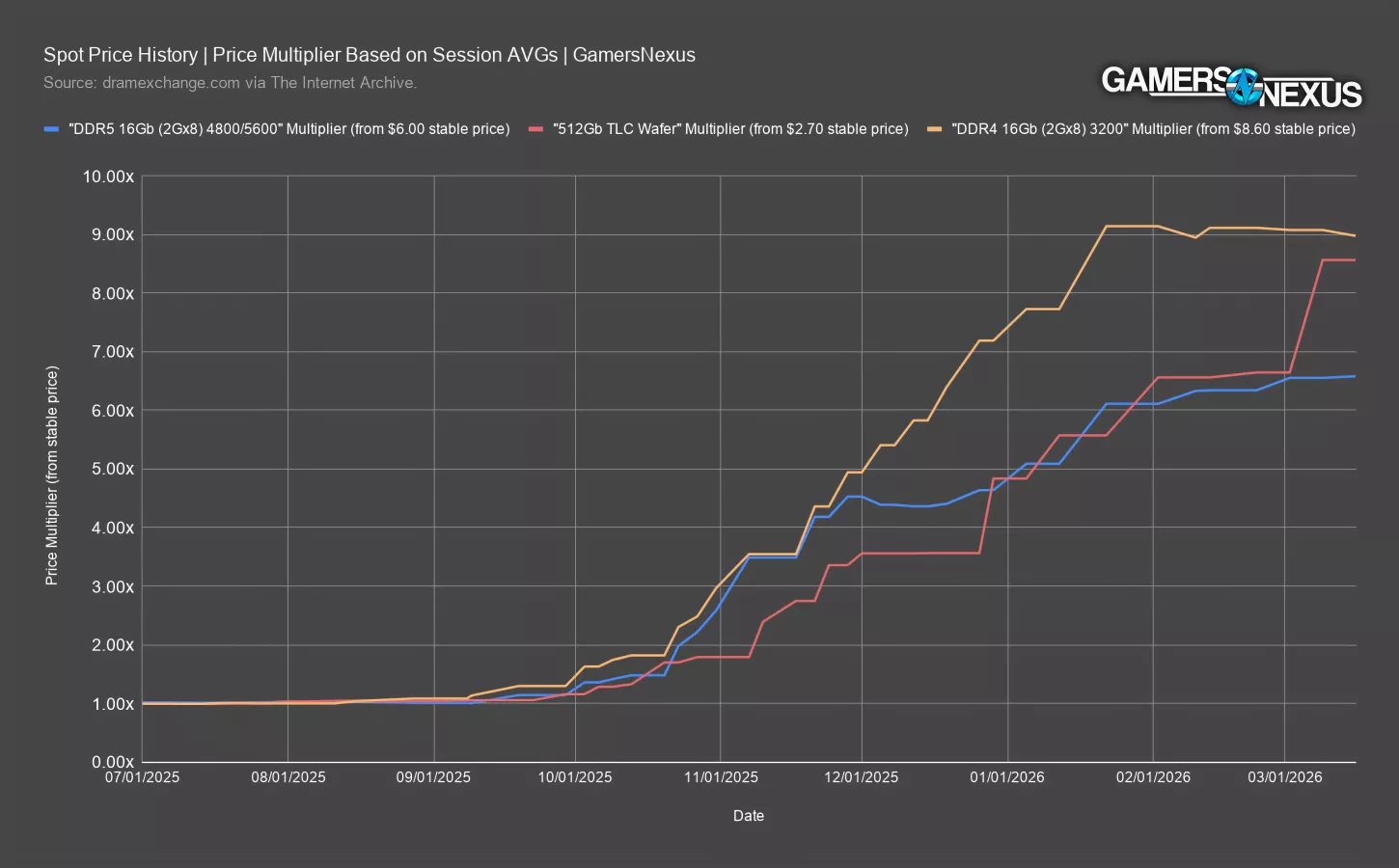

Spot Price History - Multiplier

We made this chart to identify the rate of price increases, which is comparable among entries.

Here, we’ve plotted the price multiplier rather than the actual dollar amount. Each entry’s price multiplier is relative to its own previously stable price, held between July and September last year.

DDR5 16Gb’s session AVG at slower speeds surpassed its previously stable price by 2x just before November, exceeded both 3x and then 4x in November (which is when we made our RAM: WTF? video), and shot 5x and 6x past its previously stable price in January, gradually increasing since. It currently is approaching a 7x multiplier.

SSDs are far worse.

512Gb TLC session AVG prices broke 2x and then 3x past its previously stable price by November, plateaued in December, then jumped to 6.56x by early February, pushing the % of its increases just past DDR5’s, before widening the gap further in early March when it spiked to 8.57x its previously stable price.

DDR4 16Gb’s price multiplier initially mimicked DDR5’s, surpassing 2x in mid-October, 3x in early November, and 4x in mid-November, before diverting paths and rapidly climbing to around 9x its previously stable price currently.

While DDR5 RAM kits still hold greater % increases compared to SSDs in terms of current market pricing for completed products to end users, our understanding is that SSD market prices will eventually exceed DDR5’s percent increases as the market reflects these recent changes. Some of the reason for this lag could be buffer supply and people being slower to notice and therefore slower to stockpile.

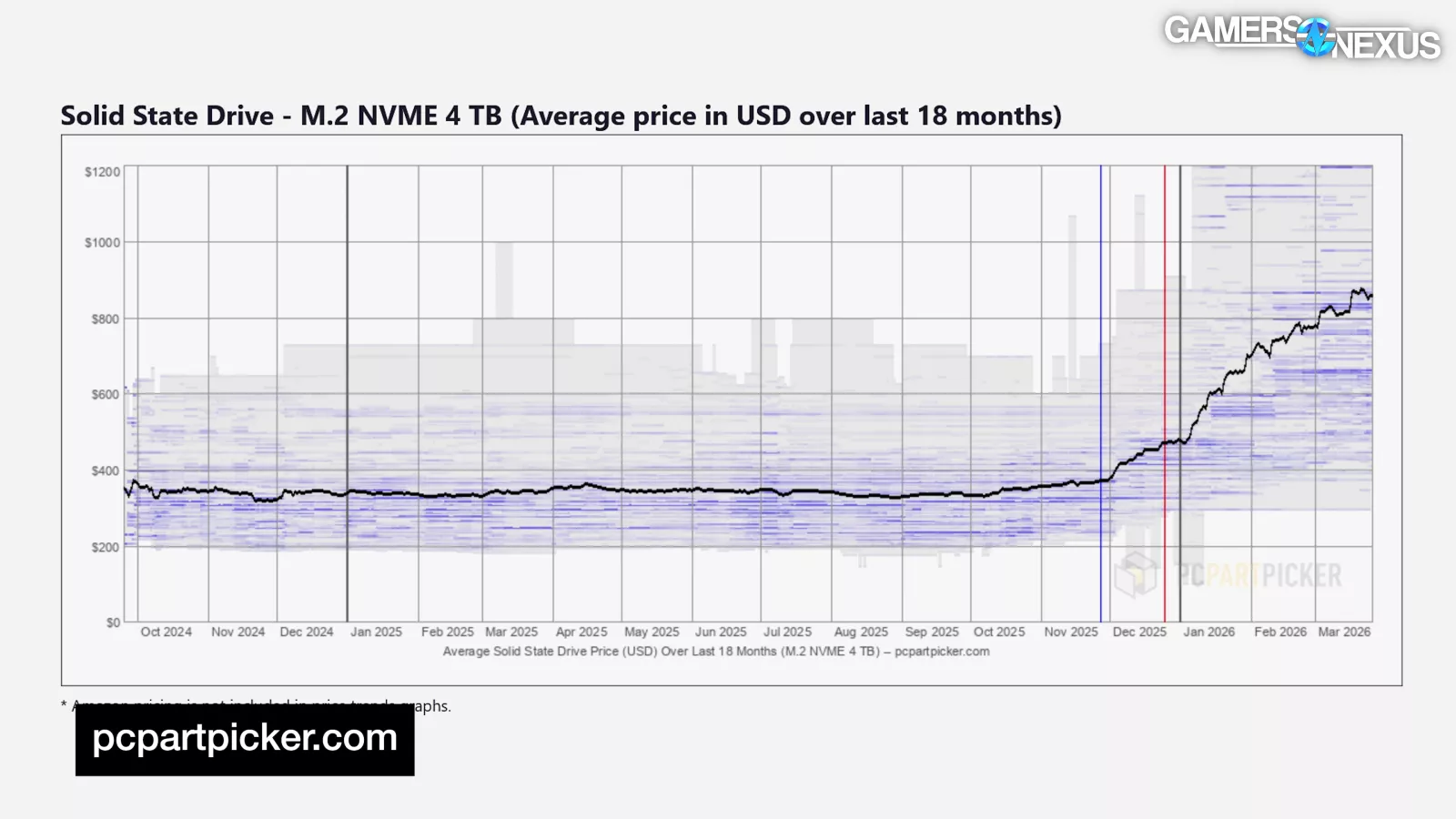

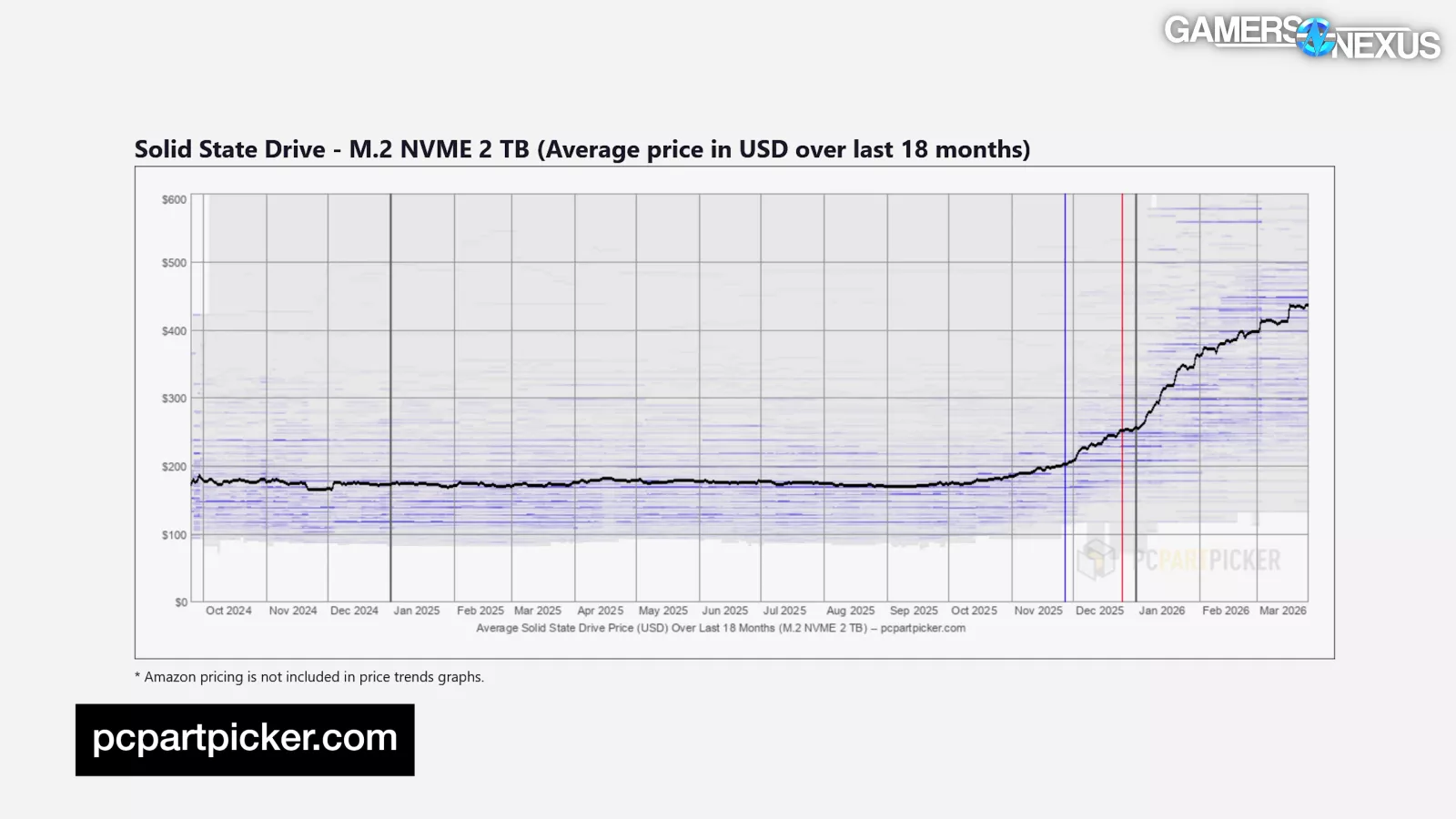

Price Trends - 2TB NVME SSD

| SSD Price Trend | M.2 NVMe SSD (2 TB) | GamersNexus11/12/2025 to 03/12/2026 | |||

| 2 TB NVMe SSDs (M.2 PCIe 4.0 X4) | Price (11/12) | Price (03/12) | Price Increase (%) |

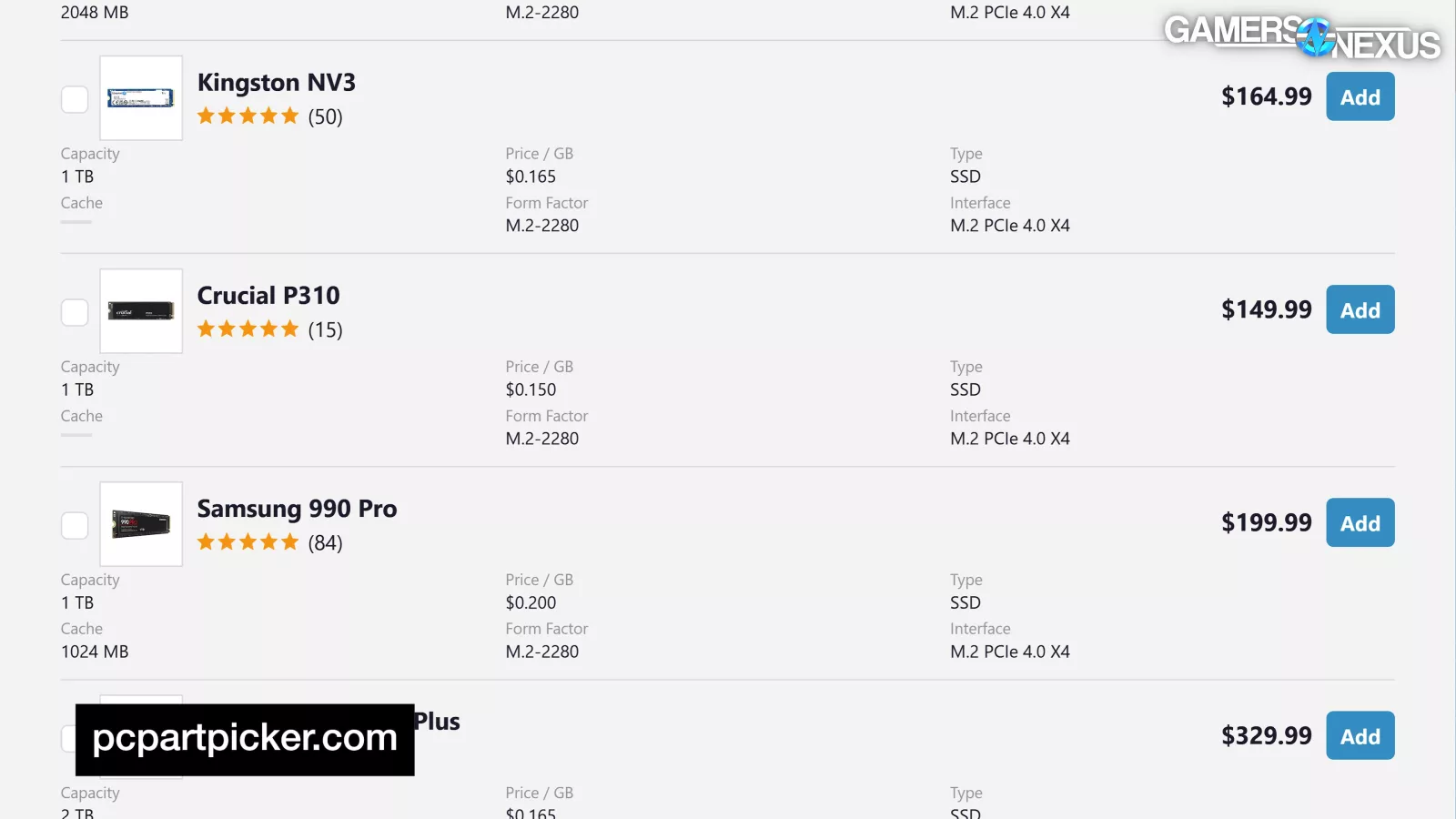

| Crucial P310 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD | $145.00 | $300.00 | 106.9% |

| WD_Black SN850X 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD | $190.00 | $350.00 | 84.2% |

| Kingston NV3 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD | $150.00 | $380.00 | 153.3% |

| Samsung 990 Pro 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD | $190.00 | $400.00 | 110.5% |

| Averages | $168.75 | $357.50 | 113.7% |

| Note: Collected Newegg prices using PC Part Picker's "Price History" |

In this table, we’ve collected Newegg prices for a couple of the most popular 2TB M.2 NVMe SSDs we could find, compiled using PC Part Picker’s “Price History” charts.

This means that we’re now looking at completed product pricing, which could use different supply than the prior table and also has other product cost factors.

Since November, Crucial’s P310 rose from $145 to $300, making it the lowest priced entry at the time of writing on this table.

Micron recently exited the direct-sale memory business (as in, RAM) for its Crucial line, so there are some other company decisions contributing here.

Western Digital’s SN850X increased from $190 to $350, or by 84.2%, representing the lowest percent increase.

Kingston’s NV3 experienced the greatest surge by both absolute cost and percent increase, swelling from $150 to $380, or by 153%.

Finally, Samsung’s 990 Pro more than doubled in price from $190 to $400, making it the highest priced entry and accompanied by a 111% increase.

Of course, there are more expensive SSDs out there, but we’re trying to narrow the band of comparison.

Averaging these entries produces a collective price increase from $168.75 in November to $357.50 currently, yielding an averaged 113.7% increase in the past four months of these devices.

We were also curious about the increases for SSDs using China’s NAND Flash newcomer YMTC. We previously covered YMTC in our Rise of Chinese Memory full-length documentary.

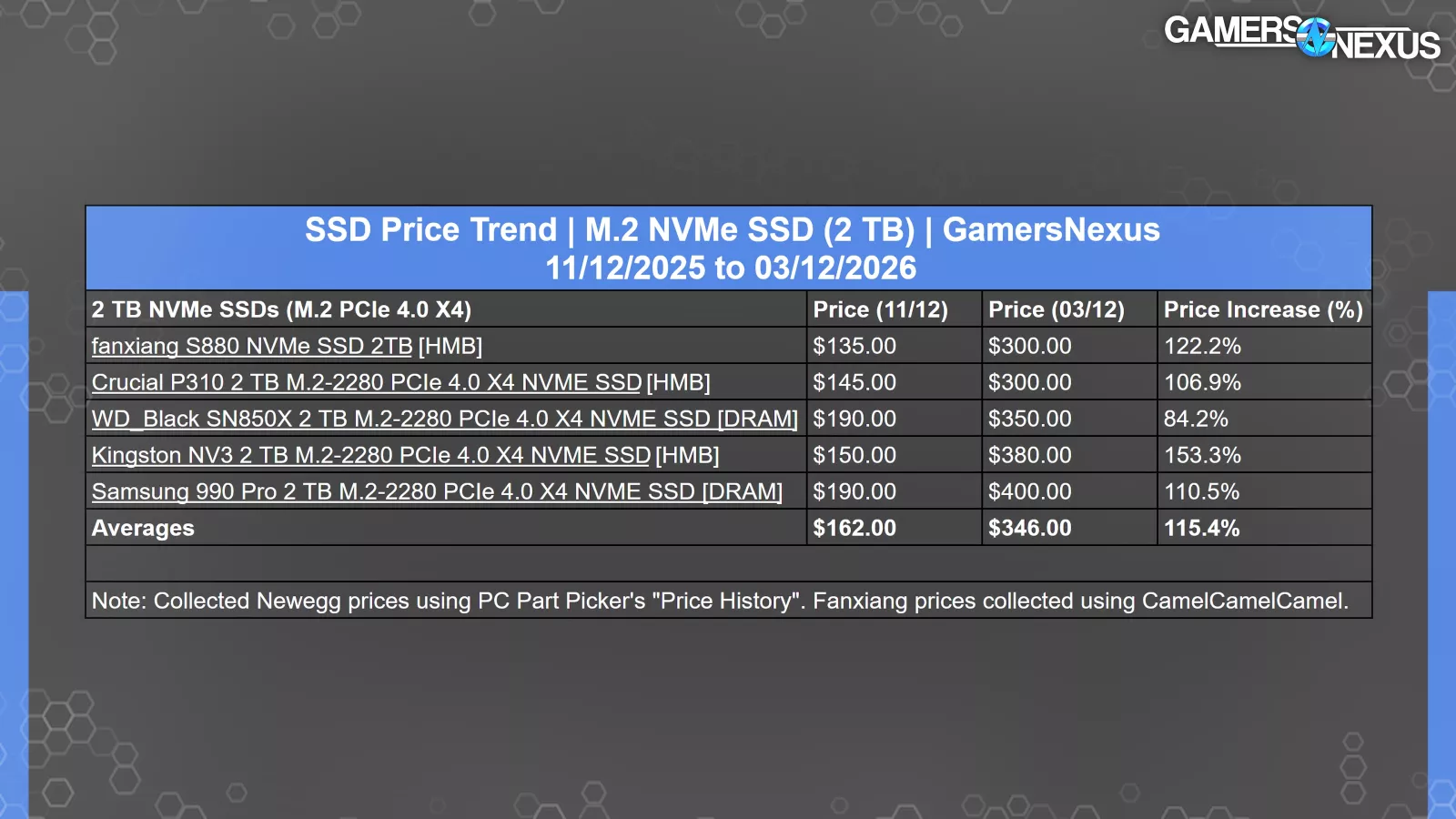

Chinese SSDs (YMTC) – Price Comparison

| SSD Price Trend | M.2 NVMe SSD (2 TB) | GamersNexus11/12/2025 to 03/12/2026 | |||

| 2 TB NVMe SSDs (M.2 PCIe 4.0 X4) | Price (11/12) | Price (03/12) | Price Increase (%) |

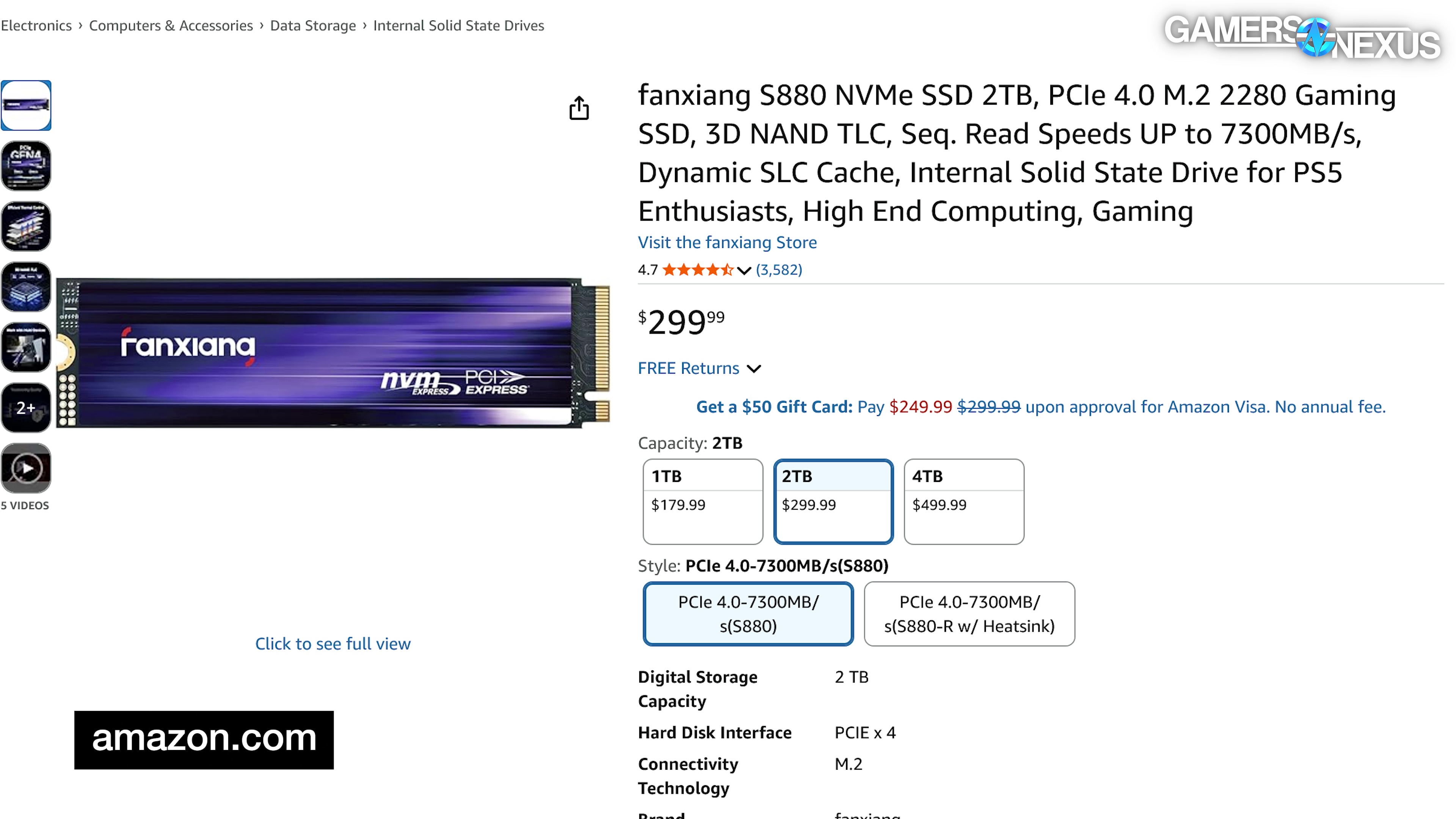

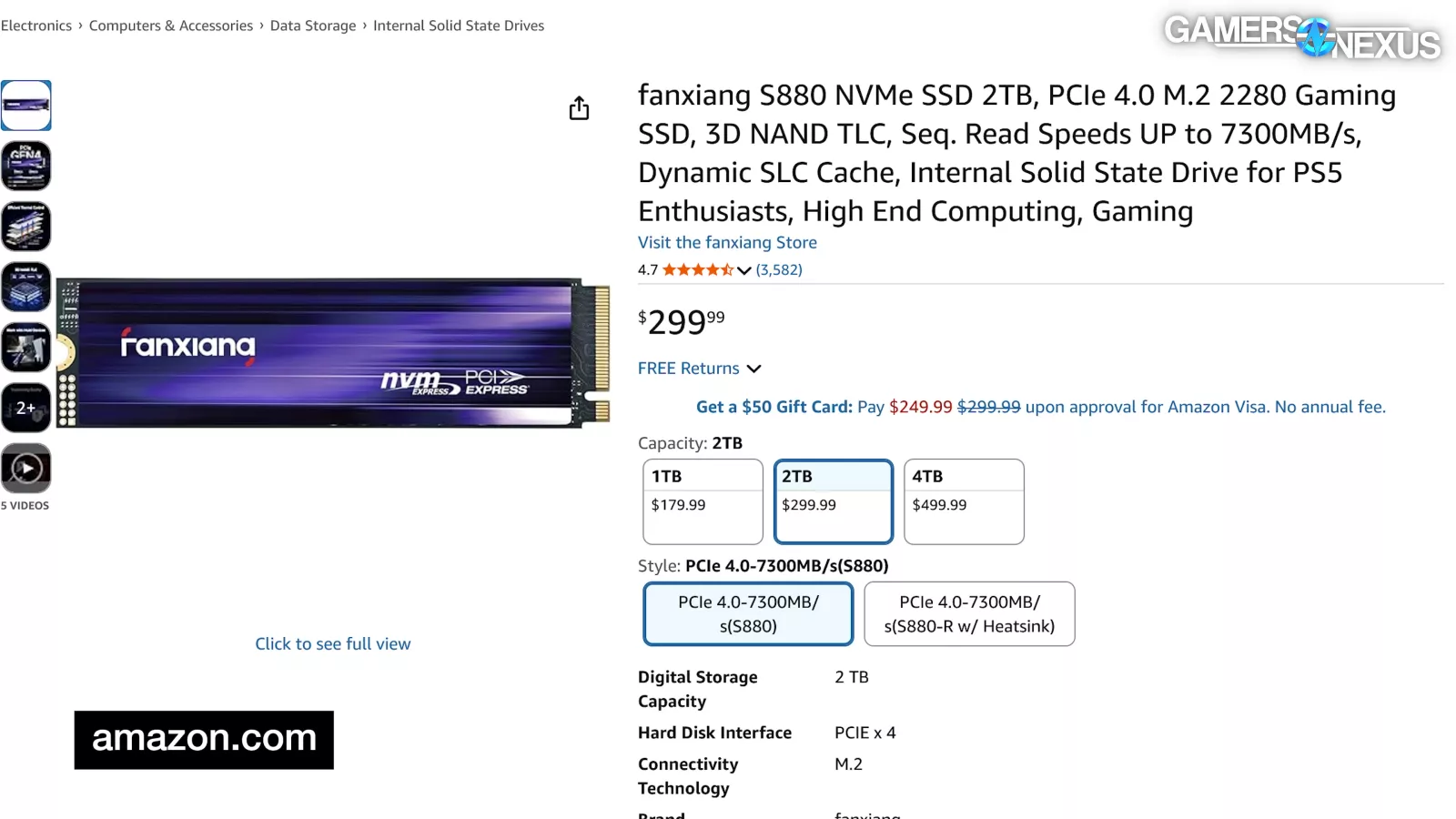

| fanxiang S880 NVMe SSD 2TB [HMB] | $135.00 | $300.00 | 122.2% |

| Crucial P310 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD [HMB] | $145.00 | $300.00 | 106.9% |

| WD_Black SN850X 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD [DRAM] | $190.00 | $350.00 | 84.2% |

| Kingston NV3 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD [HMB] | $150.00 | $380.00 | 153.3% |

| Samsung 990 Pro 2 TB M.2-2280 PCIe 4.0 X4 NVME SSD [DRAM] | $190.00 | $400.00 | 110.5% |

| Averages | $162.00 | $346.00 | 115.4% |

| Note: Collected Newegg prices using PC Part Picker's "Price History". Fanxiang prices collected using CamelCamelCamel. |

This is the same chart of 2TB drives, but with YMTC supply added.

The Fanxiang S880, using YMTC NAND, is comparable to each entry by advertised read/write speeds. We have not tested these devices to validate the claims, but did check the marketing spec sheet for the comparisons.

We’ve also added labels to indicate which SSDs use a host memory buffer vs those possessing a DRAM cache. Hypothetically, SSDs with a DRAM cache would have a higher cost impact than those without thanks to the DRAM pricing surge.

As seen in our chart above, with an over 120% increase since November, SSDs using YMTC NAND are apparently unable to avoid the outrageous surges. YMTC or Fanxiang are capitalizing on this in much the same way as their other competitors.

That being said, the Fanxiang SSD held the lowest price in November by absolute price of these and is tied for the lowest price currently. The drive is between $80 and $100 less than the two highest priced entries on this table, so it still appears to offer competitive pricing despite its recent increases.

YMTC also recently released its first PCIE 5.0 compliant NVMe drive, built on its in-house Xtacking 4.0 architecture, signaling its ability to remain developmentally competitive with other manufacturers' progression for the latest PCIe generation.

Xtacking requires two wafers, so is a wafer-expensive approach to manufacturing that yields greater density.

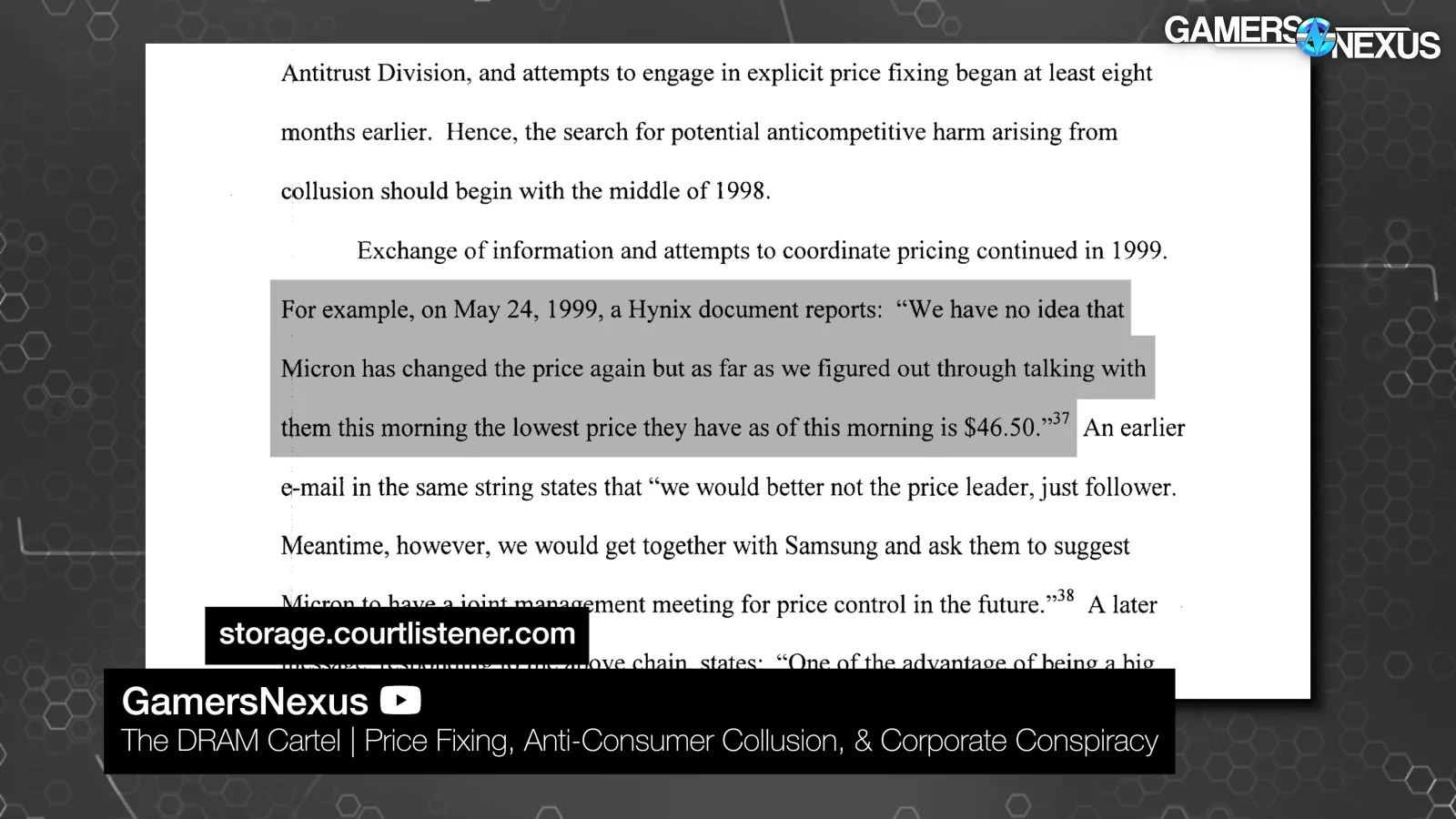

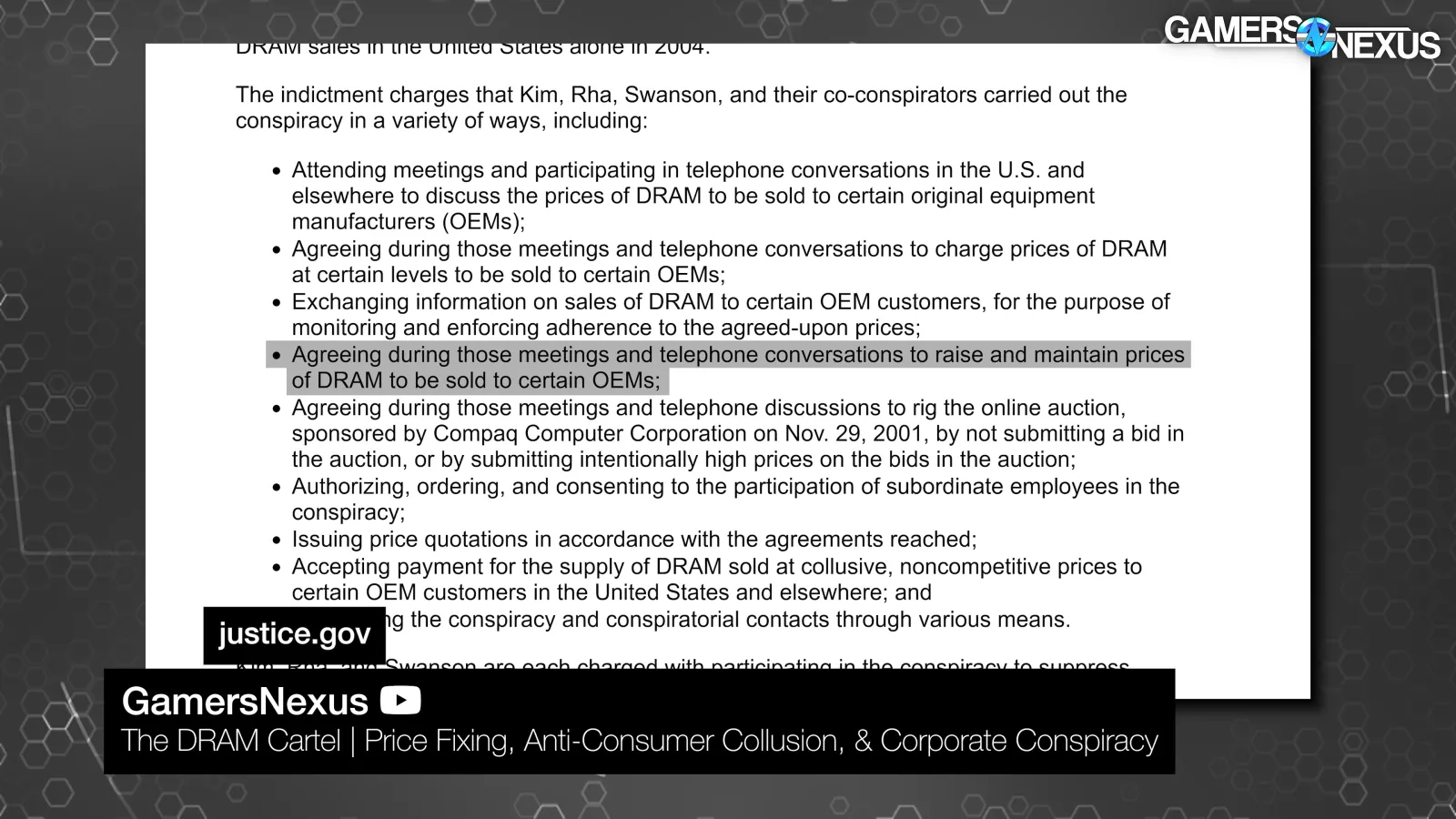

You should check out our “Rise of Chinese Memory” video for more information on YMTC and its recent expansion, but we ultimately remain optimistic about what a growing manufacturer means for the industry amidst the shortage. It makes it more difficult for companies to collude (hopefully), especially as more cultures are introduced. Related to that, we have another documentary called “The DRAM Cartel” where we cover the pricing collusion of American and Korean manufacturers of the past.

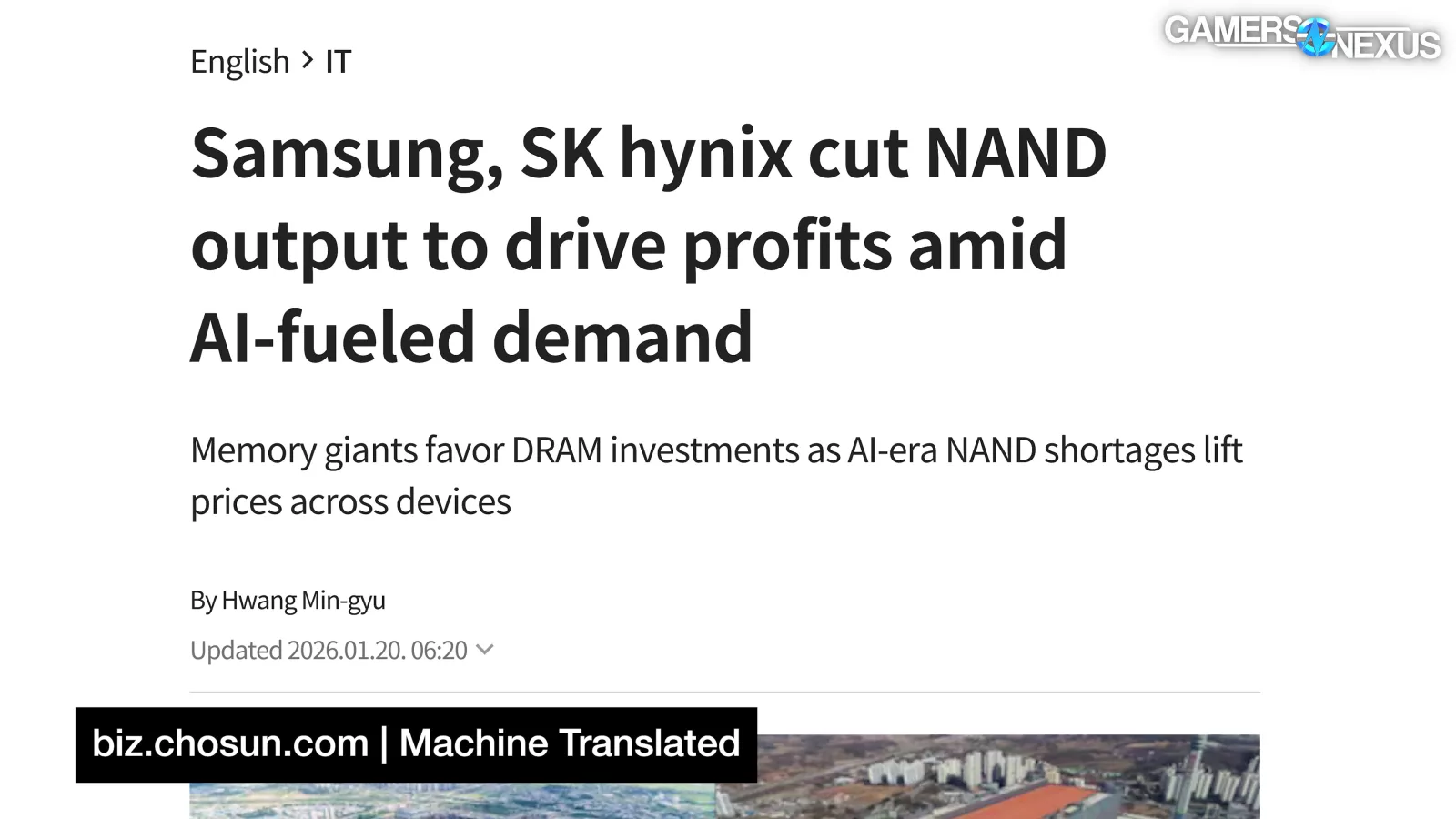

In January, Chosun Biz, citing Omdia, reported that both Samsung and SK Hynix lowered NAND wafer output from 2025 to 2026, adding (through machine translation):

“Some also say the move reflects awareness that supply of commodity Chinese NAND is increasing. Unlike Samsung Electronics and SK hynix, China's YMTC has been raising its profile in the NAND market since last year and steadily increasing volume. To counter low-priced competition from China, the companies appear intent on reducing NAND supply to mobile and PCs to defend profitability, while increasing server and enterprise volumes to manage the production mix.”

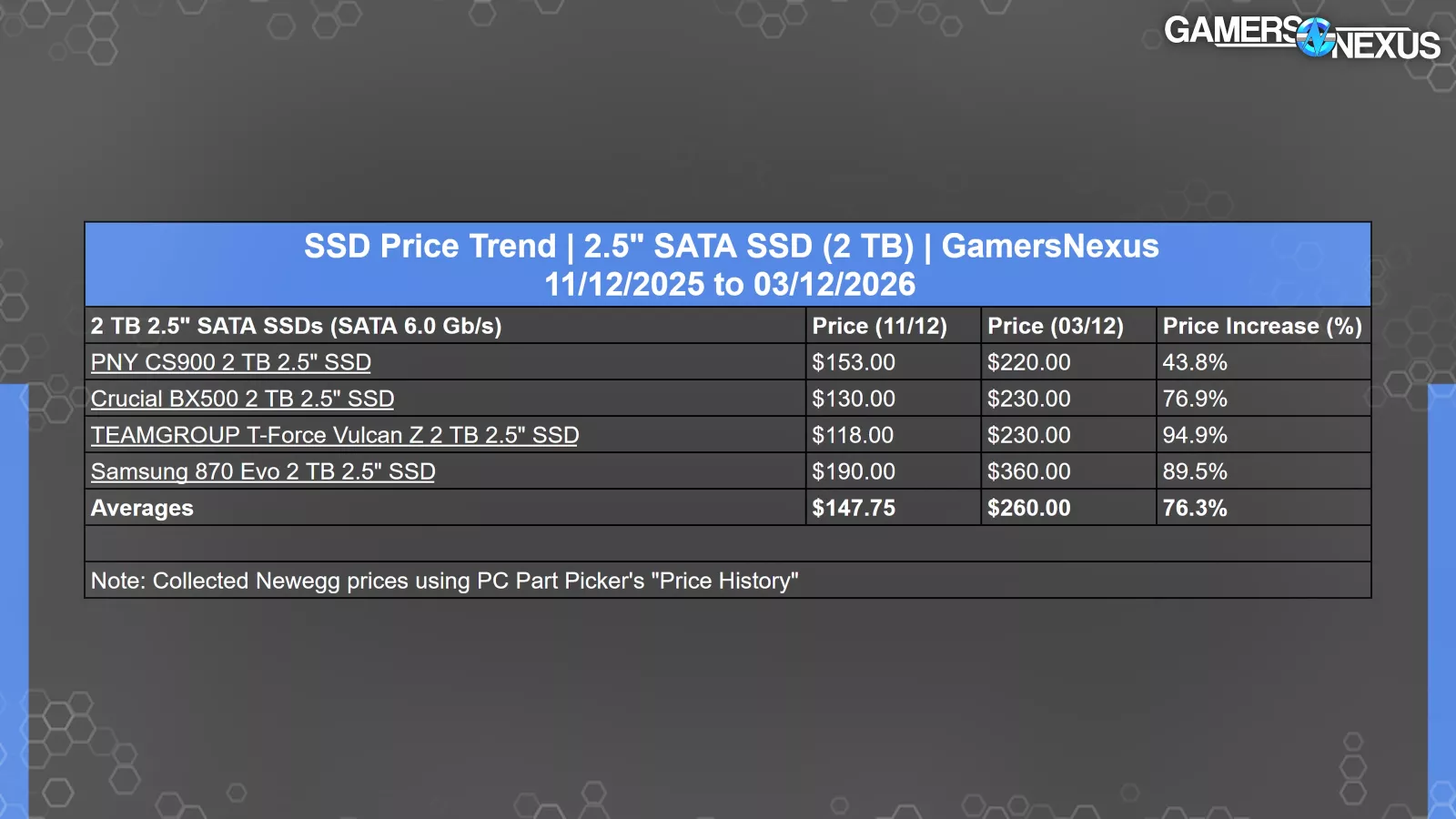

Price Trends - 2TB SATA SSD

| SSD Price Trend | 2.5" SATA SSD (2 TB) | GamersNexus11/12/2025 to 03/12/2026 | |||

| 2 TB 2.5" SATA SSDs (SATA 6.0 Gb/s) | Price (11/12) | Price (03/12) | Price Increase (%) |

| PNY CS900 2 TB 2.5" SSD | $153.00 | $220.00 | 43.8% |

| Crucial BX500 2 TB 2.5" SSD | $130.00 | $230.00 | 76.9% |

| TEAMGROUP T-Force Vulcan Z 2 TB 2.5" SSD | $118.00 | $230.00 | 94.9% |

| Samsung 870 Evo 2 TB 2.5" SSD | $190.00 | $360.00 | 89.5% |

| Averages | $147.75 | $260.00 | 76.3% |

| Note: Collected Newegg prices using PC Part Picker's "Price History" |

This table plots the same data but instead focuses on the most commonly used 2.5” SATA SSDs we could find price histories for.

Since November, PNY’s CS900 increased from $153 to $220, or by nearly 44%.

TeamGroup’s T-Force Vulcan nearly doubled from $118 to $230, or by 95%, achieving the greatest percent increase listed.

Samsung’s 870 Evo rose from $190 to $360, or by $170, granting it the greatest absolute increase.

Collectively, the AVG price of these listings inflated from around $148 in November to $260 currently, yielding an average 76.3% increase within a four-month span.

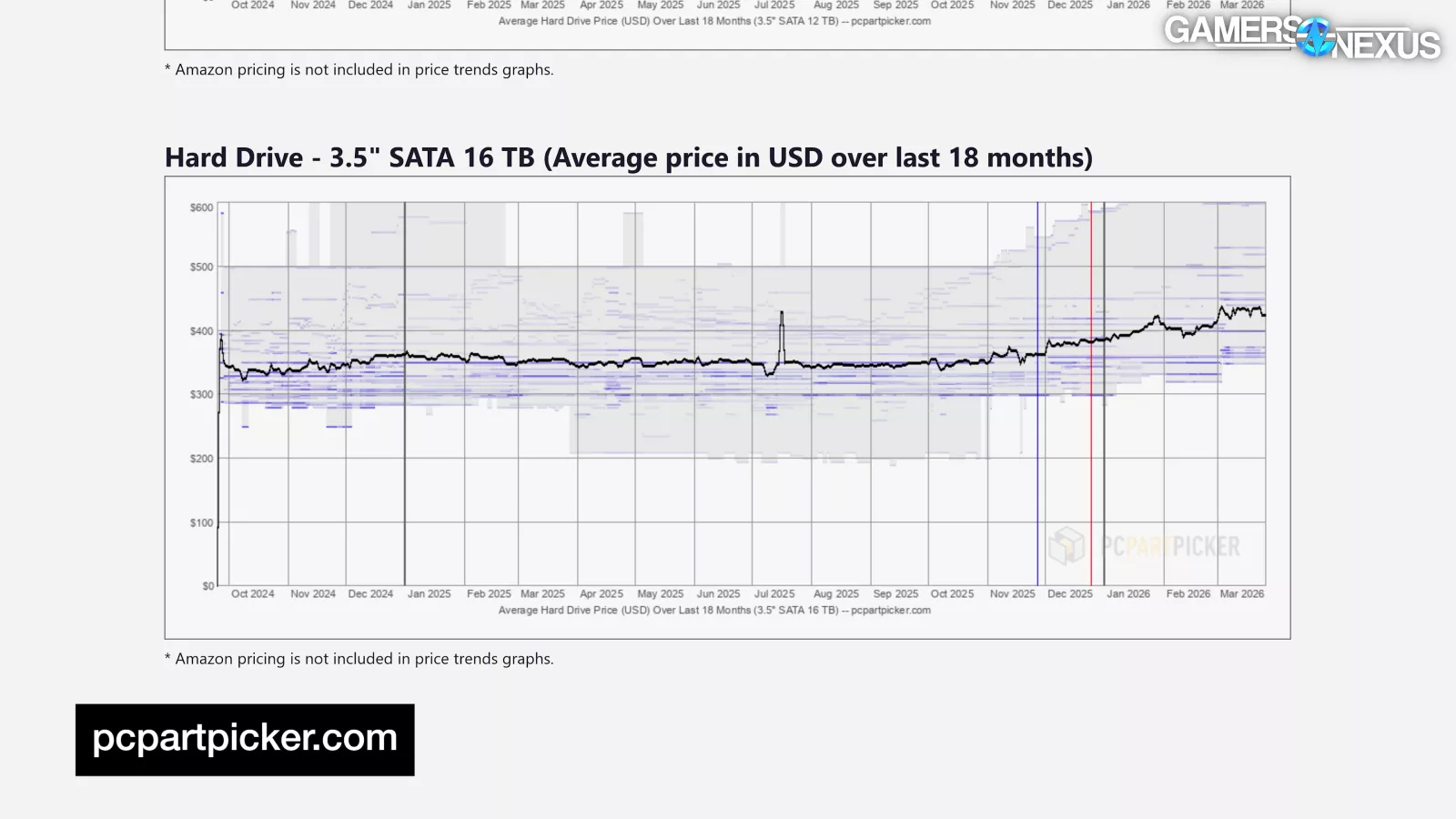

Price Trends - 16TB HDD

Hard drives don’t use NAND. They use platters, or spinning disks, aka “spinning rust.”

Still, hard drives also have manufacturing output limitations and are in high demand for data centers.

While we didn’t find reliable price histories for any individual hard drives, we’ve decided to include PC Part Picker’s “Price Trends” chart for 3.5” SATA 16 TB hard drives.

As seen here, prices hovered around $350 for almost the entire year. Around December or so, prices gradually increased, a trend that’s continued monthly since. The average 16 TB hard drive price has climbed from $350 to $440 currently, which amounts to over a 25% increase in just a few months. This is modest compared to the over 75% SATA SSD average increase and nearly 115% NVMe SSD increases, but it’s still a noticeable price hike.

We anticipate these prices will continue to climb, especially for 20 TB and other segments desirable to data centers.

Why Prices Are Increasing

As for why the prices are increasing, we’ve broken it down into a few key elements.

The first element is a hard drive shortage forming seemingly overnight toward the end of 2025 and beginning of this year, which in turn has accelerated the data center transition towards SSDs during a time of unforeseen storage demand, which is causing pressure on the SSD market.

This PC Mag writeup from February notes that AI data centers reserved all of Western Digital’s 2026 supply, quoting Western Digital’s CEO as saying: “We’re pretty much sold out for Calendar 2026. We have firm POs with our top seven customers.” PC Mag noted 89% of WD’s revenue comes from enterprise and cloud service solutions, which would include data centers.

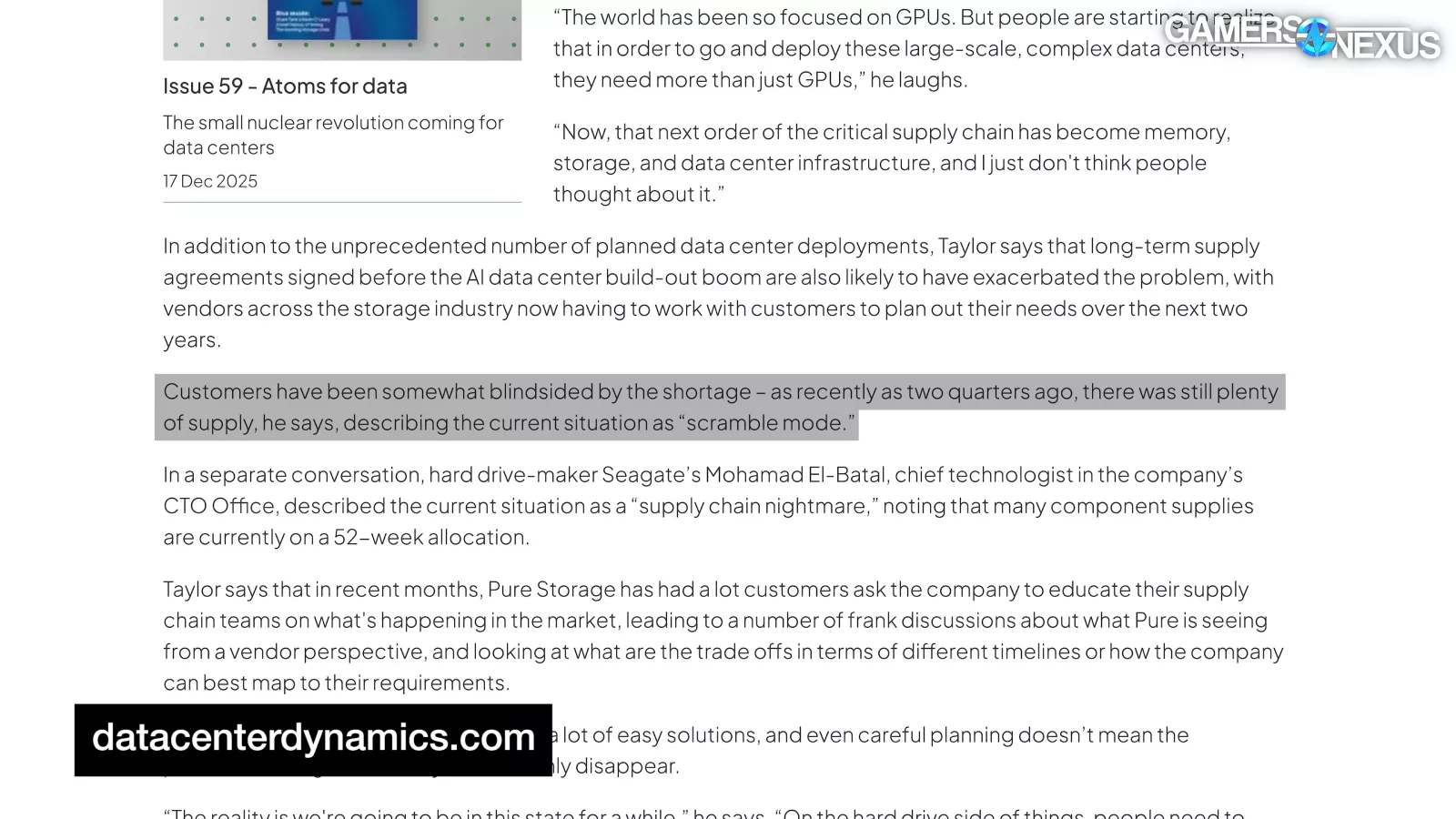

Data Center Dynamics, citing VP of storage provider Everpure (formerly Pure Storage), describes the sudden shift, explaining:

“Customers have been somewhat blindsided by the shortage – as recently as two quarters ago, there was still plenty of supply, he says, describing the current situation as ‘scramble mode.’”

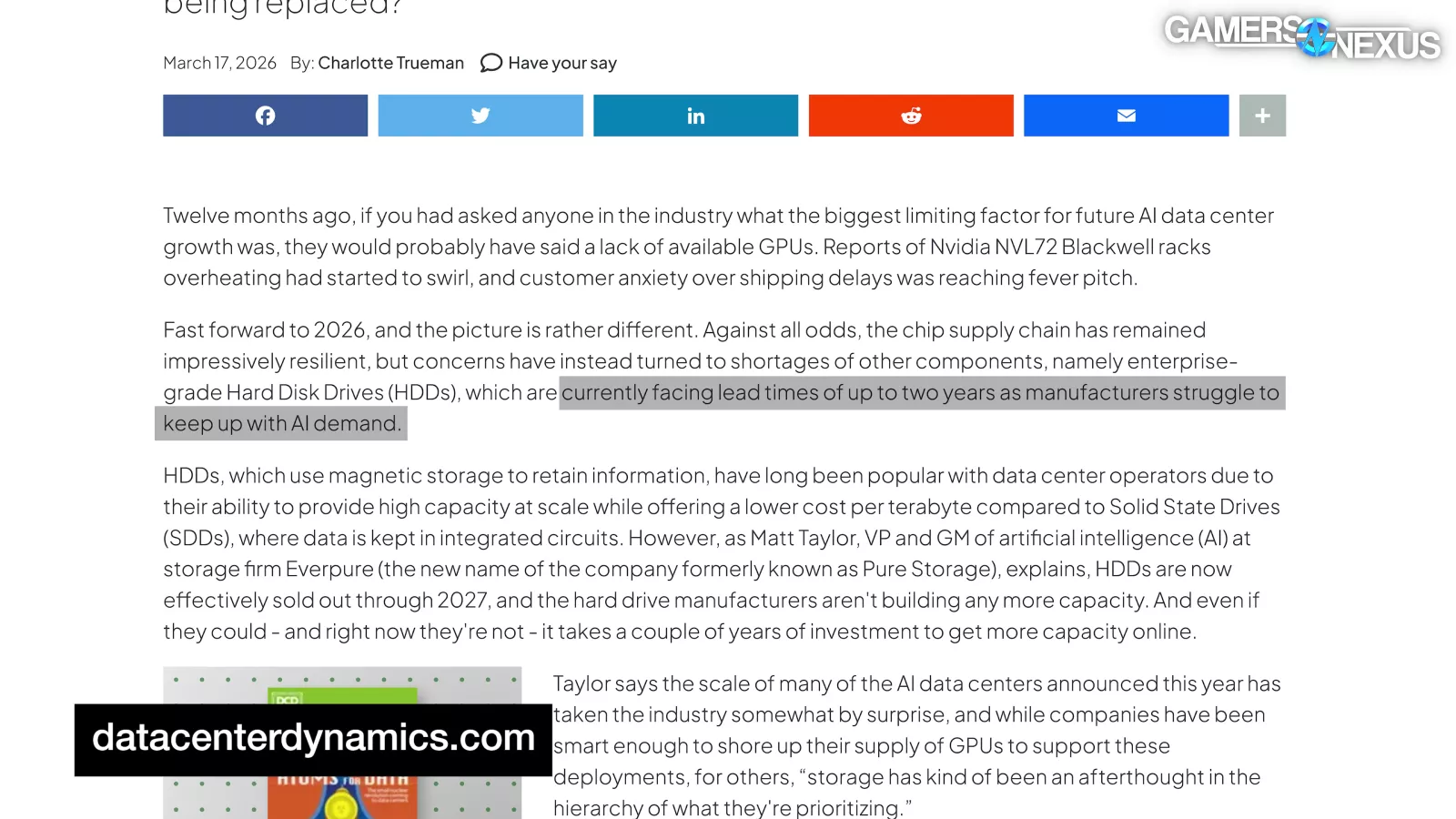

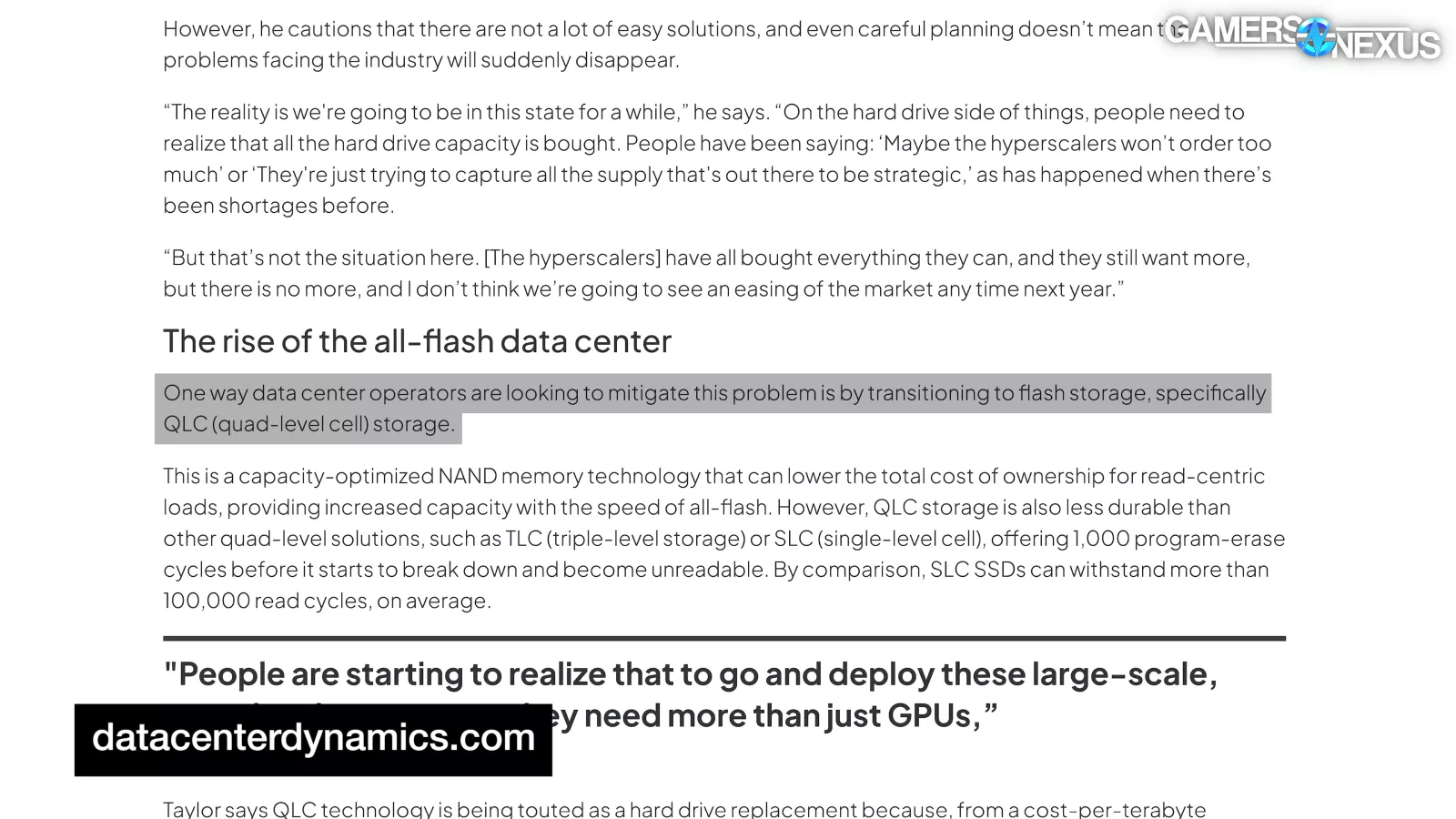

DCD’s report also claims enterprise HDDs “are currently facing lead times of up to two years as manufacturers struggle to keep up with AI demand,” and explains how “one way data center operators are looking to mitigate this problem is by transitioning to flash storage, specifically QLC (quad-level cell) storage.”

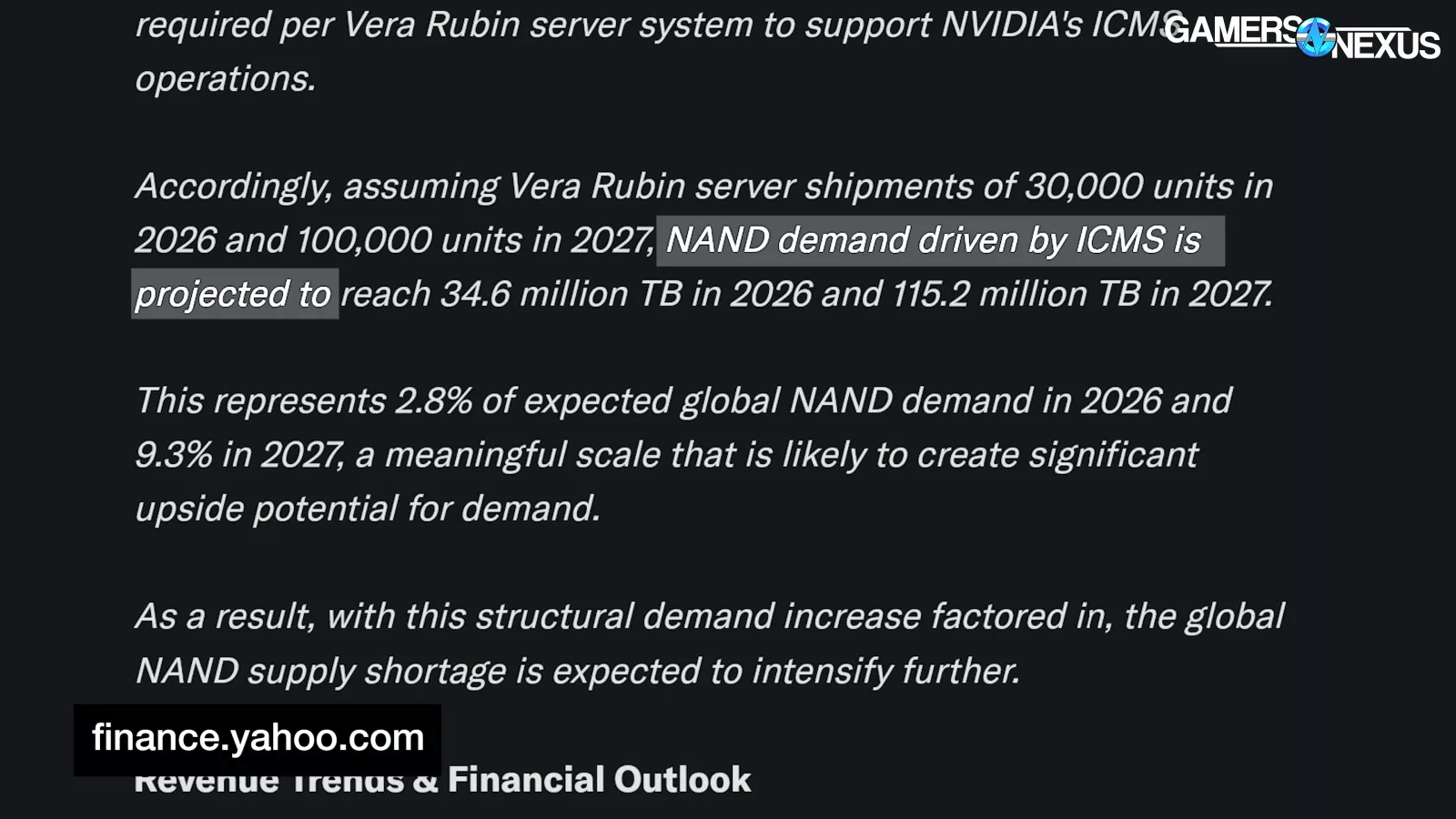

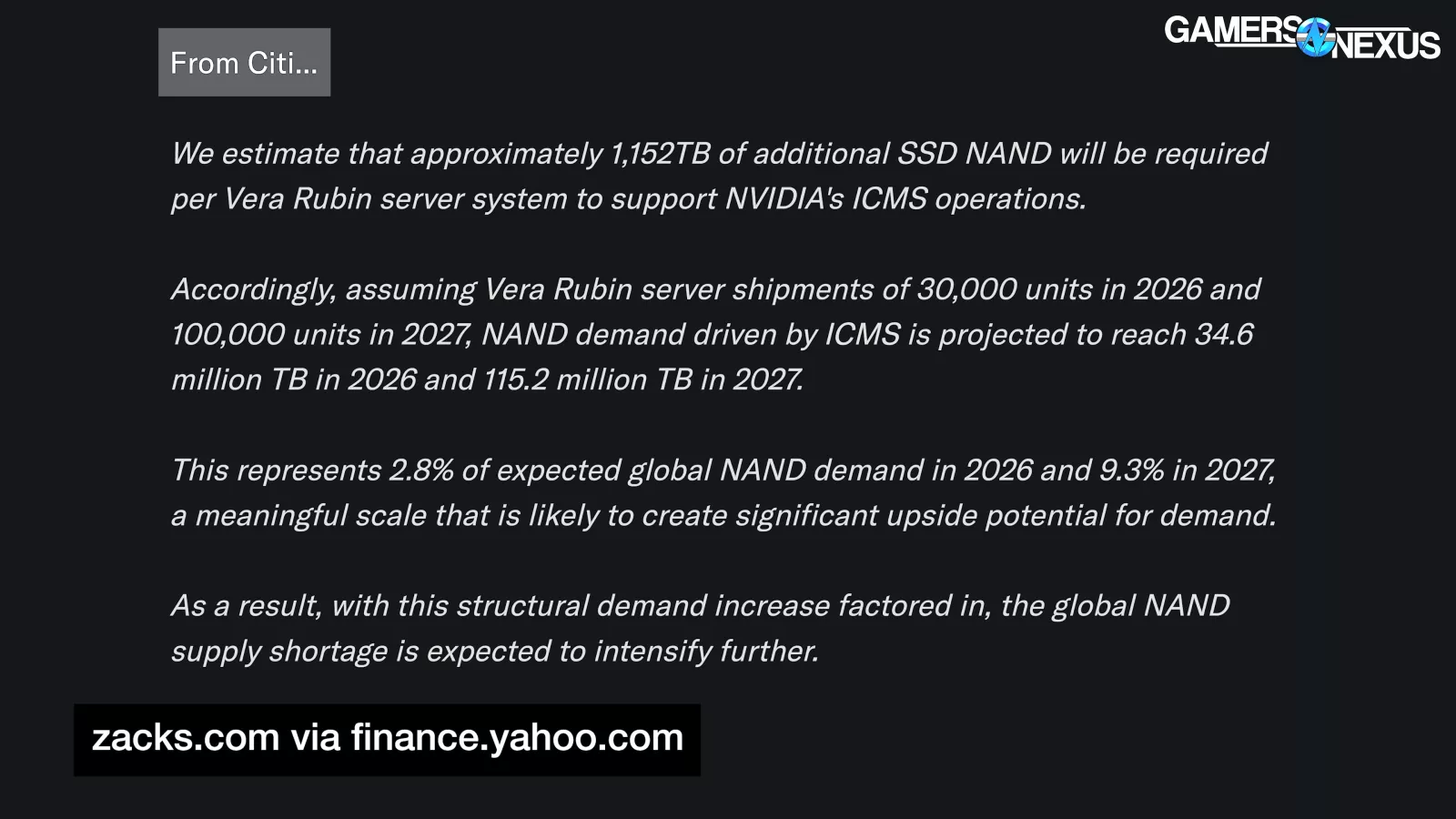

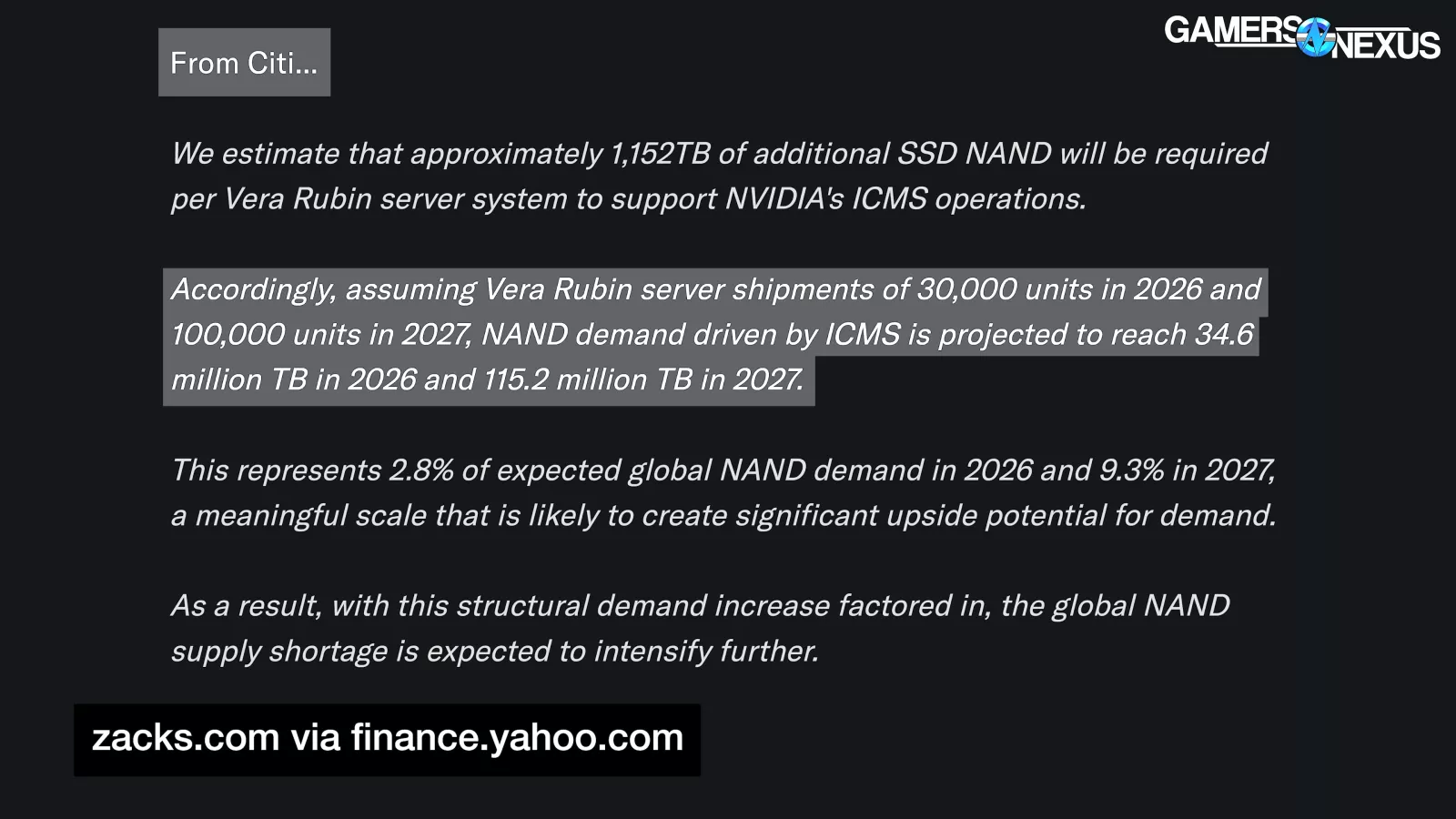

In the finance world, Citi estimates “that approximately 1,152TB of additional SSD NAND will be required per Vera Rubin server system to support NVIDIA's ICMS,” or Inference Context Memory Storage Platform. Vera Rubin is Nvidia's new server solution. So, that’s over 1 Petabyte of extra storage per Vera Rubin solution.

Citi continues:

“Accordingly, assuming Vera Rubin server shipments of 30,000 units in 2026 and 100,000 units in 2027, NAND demand driven by ICMS is projected to reach 34.6 million TB in 2026 and 115.2 million TB in 2027.

This represents 2.8% of expected global NAND demand in 2026 and 9.3% in 2027, a meaningful scale that is likely to create significant upside potential for demand.” Now to us, that climb from 2.8 to 9.3 is really the concerning part on the consumer side.

Similarly, according to Mordor Intelligence, which is somehow a real name:

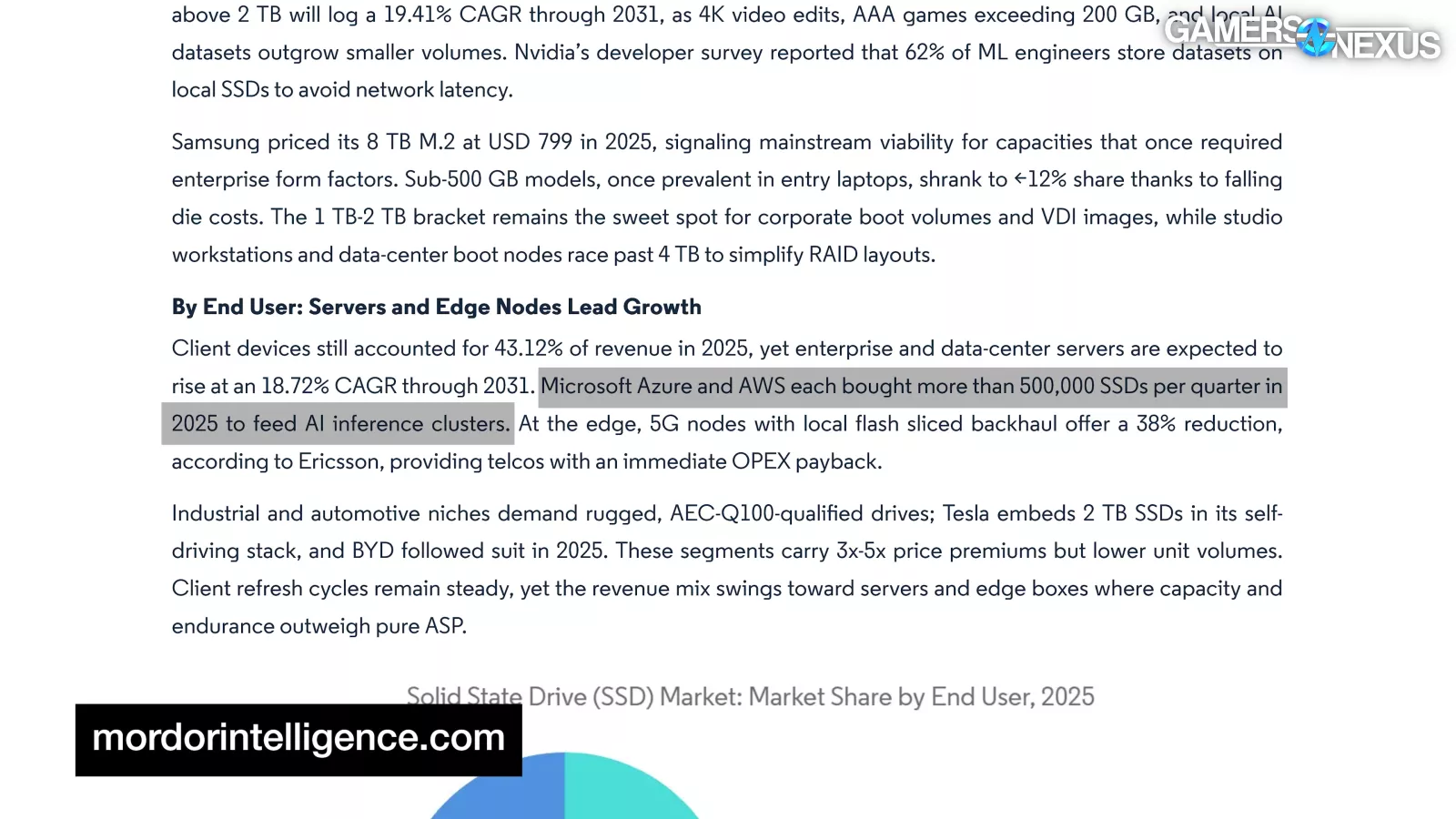

“Microsoft Azure and AWS each bought more than 500,000 SSDs per quarter in 2025 to feed AI inference clusters.”

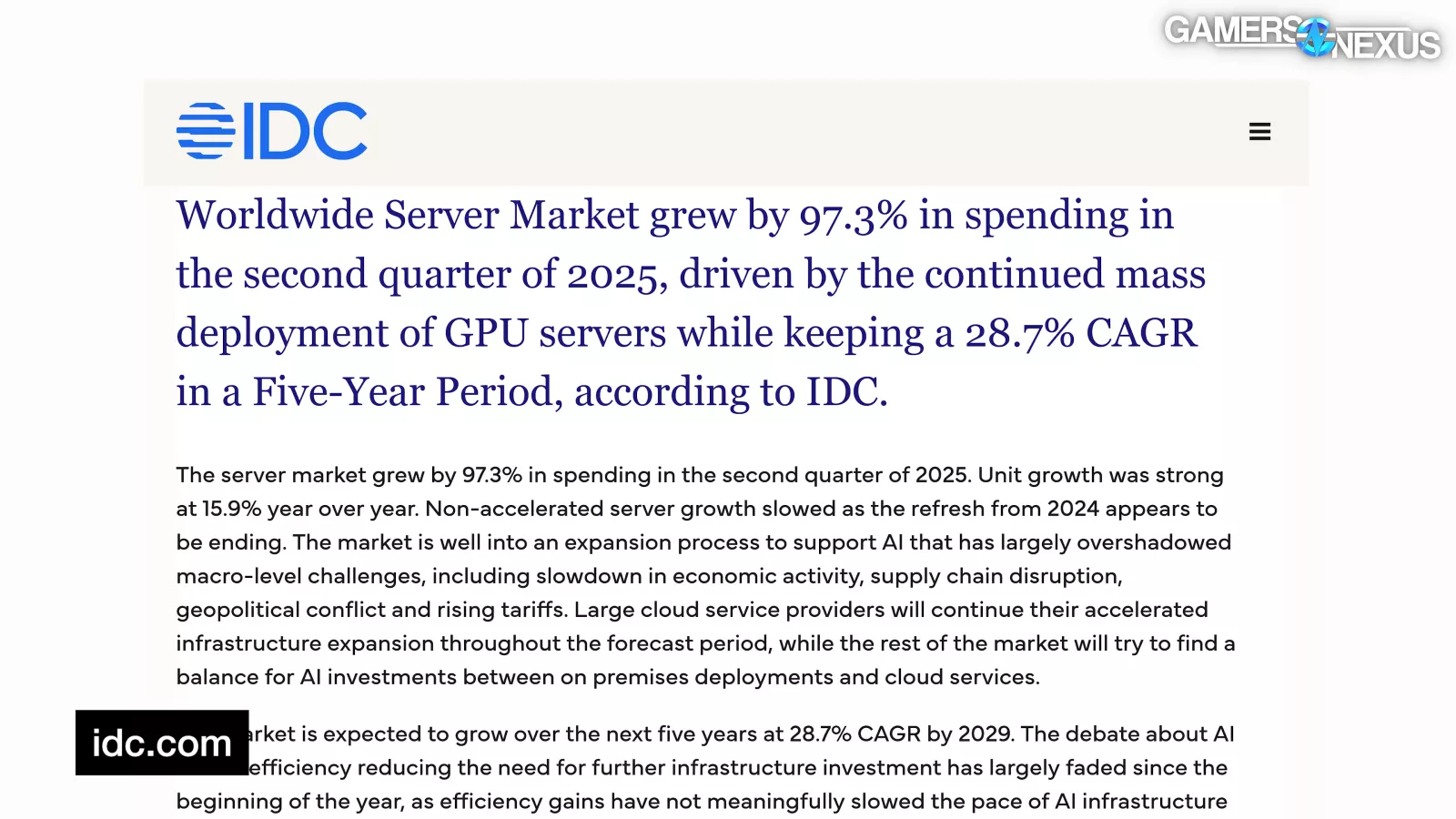

The IDC reports that the “Worldwide Server Market grew by 97.3% in spending in the second quarter of 2025.”

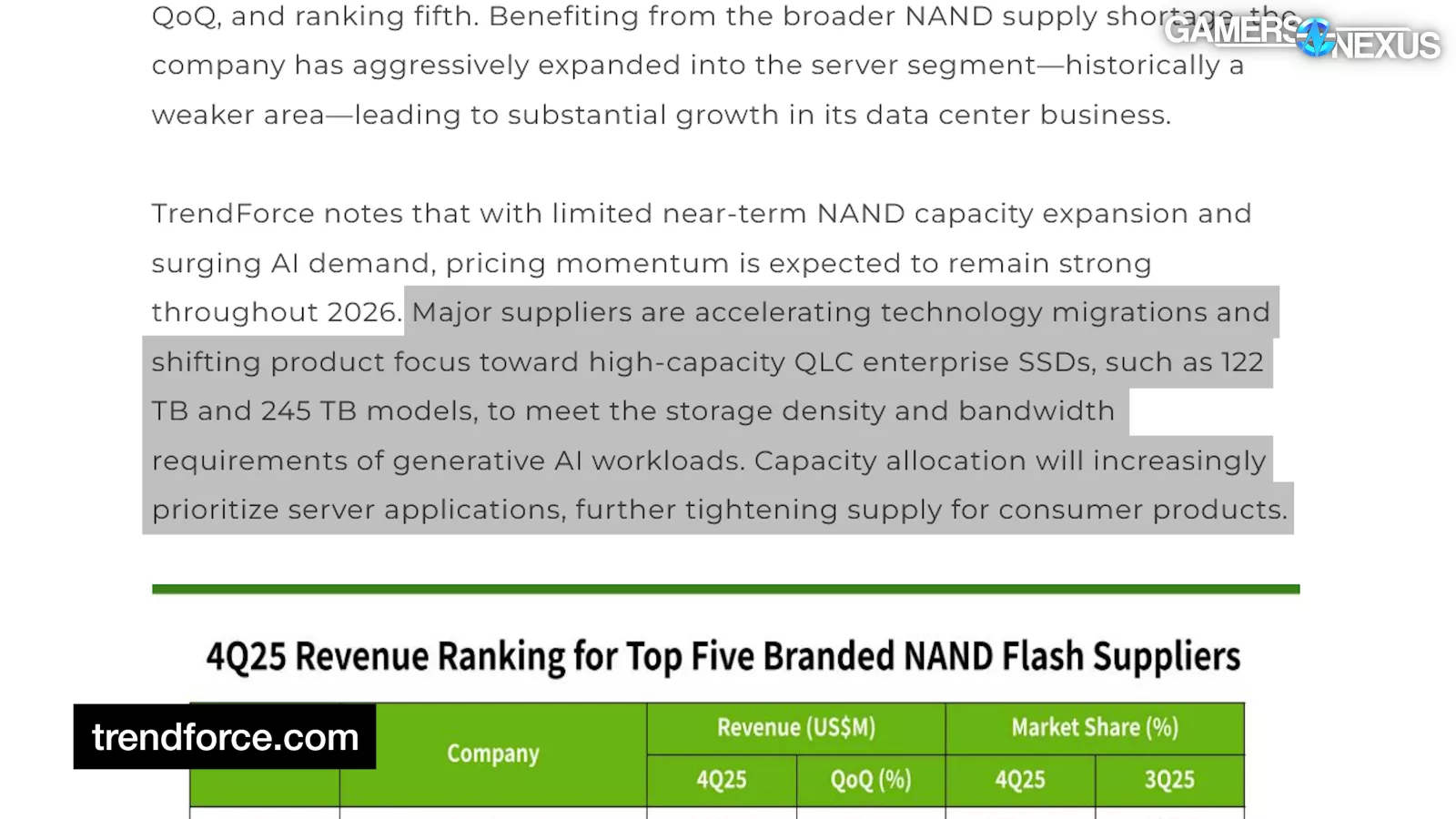

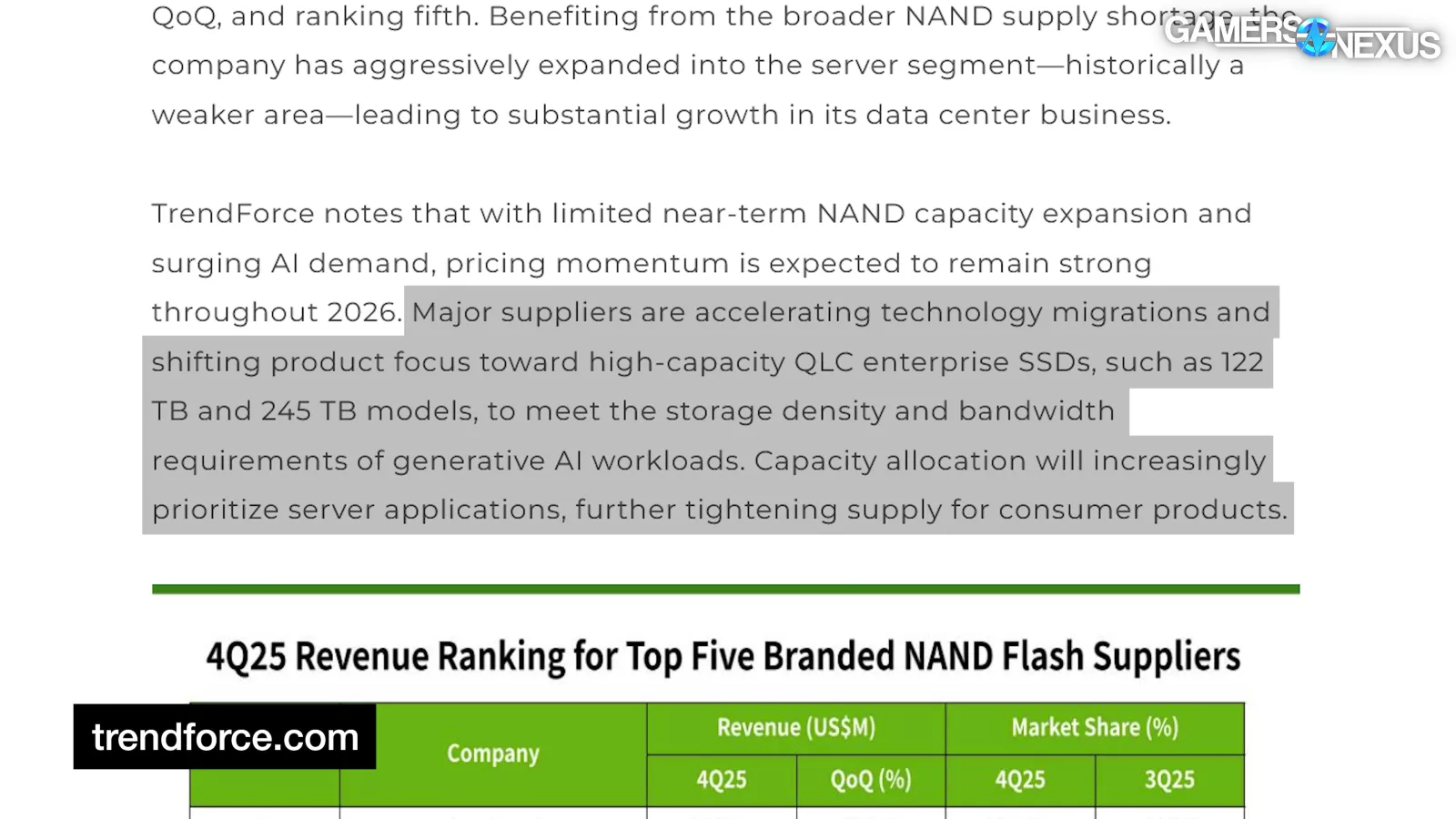

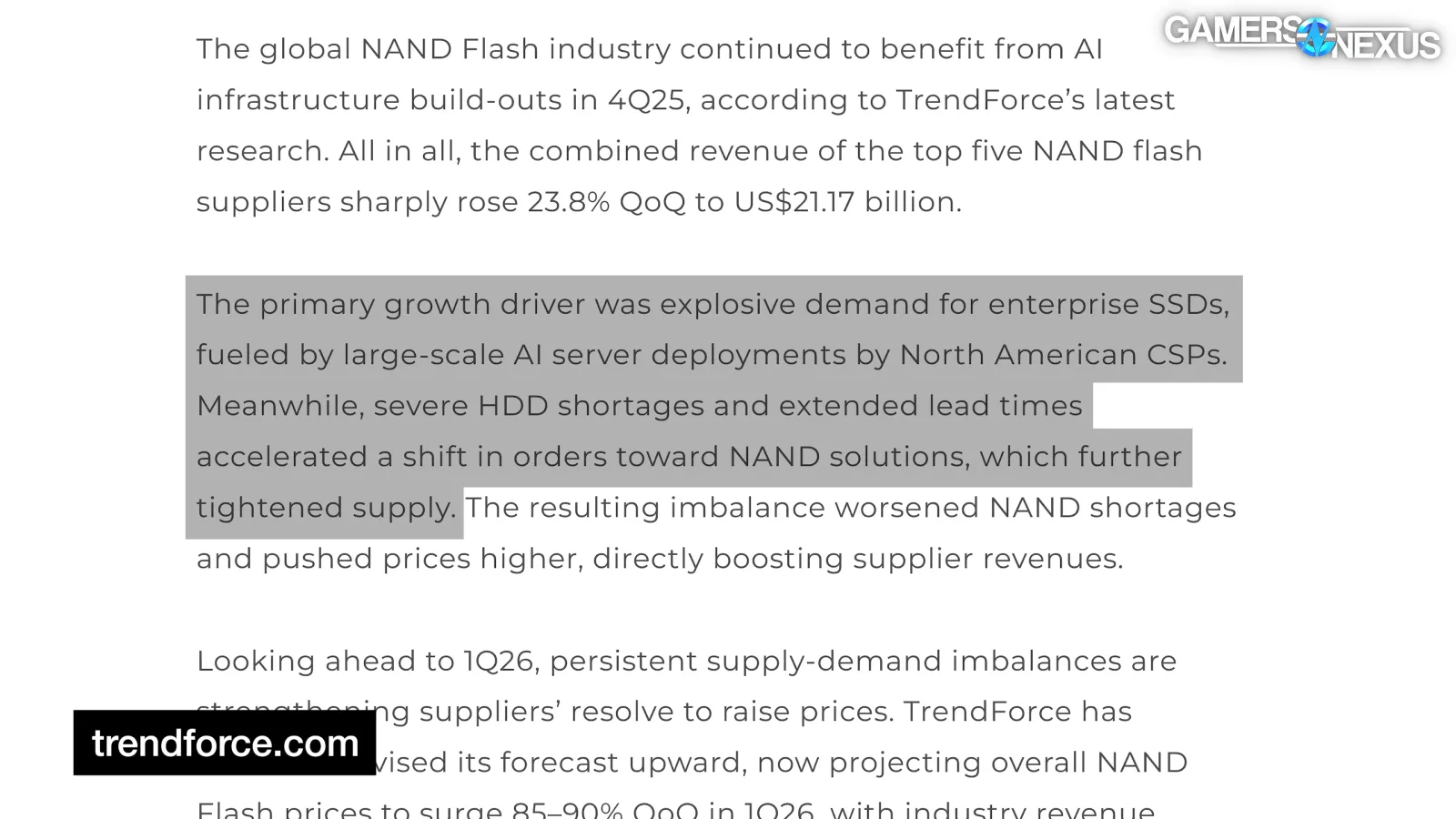

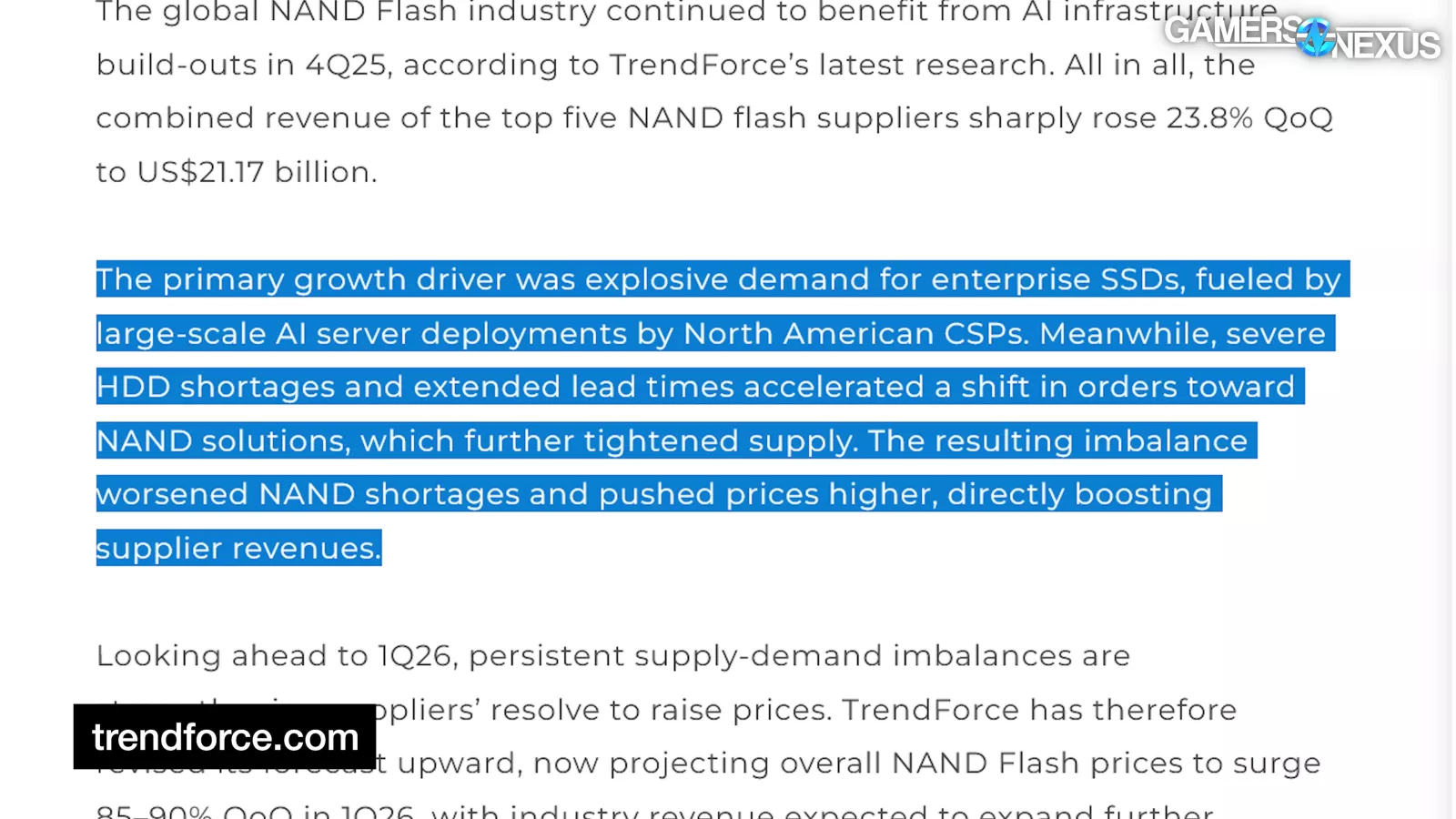

Naturally, the NAND manufacturers have begun shifting production capacity away from consumer SSDs and instead towards higher-margin enterprise SSDs, which TrendForce supports, reporting:

“The primary growth driver was explosive demand for enterprise SSDs, fueled by large-scale AI server deployments by North American CSPs. Meanwhile, severe HDD shortages and extended lead times accelerated a shift in orders toward NAND solutions, which further tightened supply.”

And:

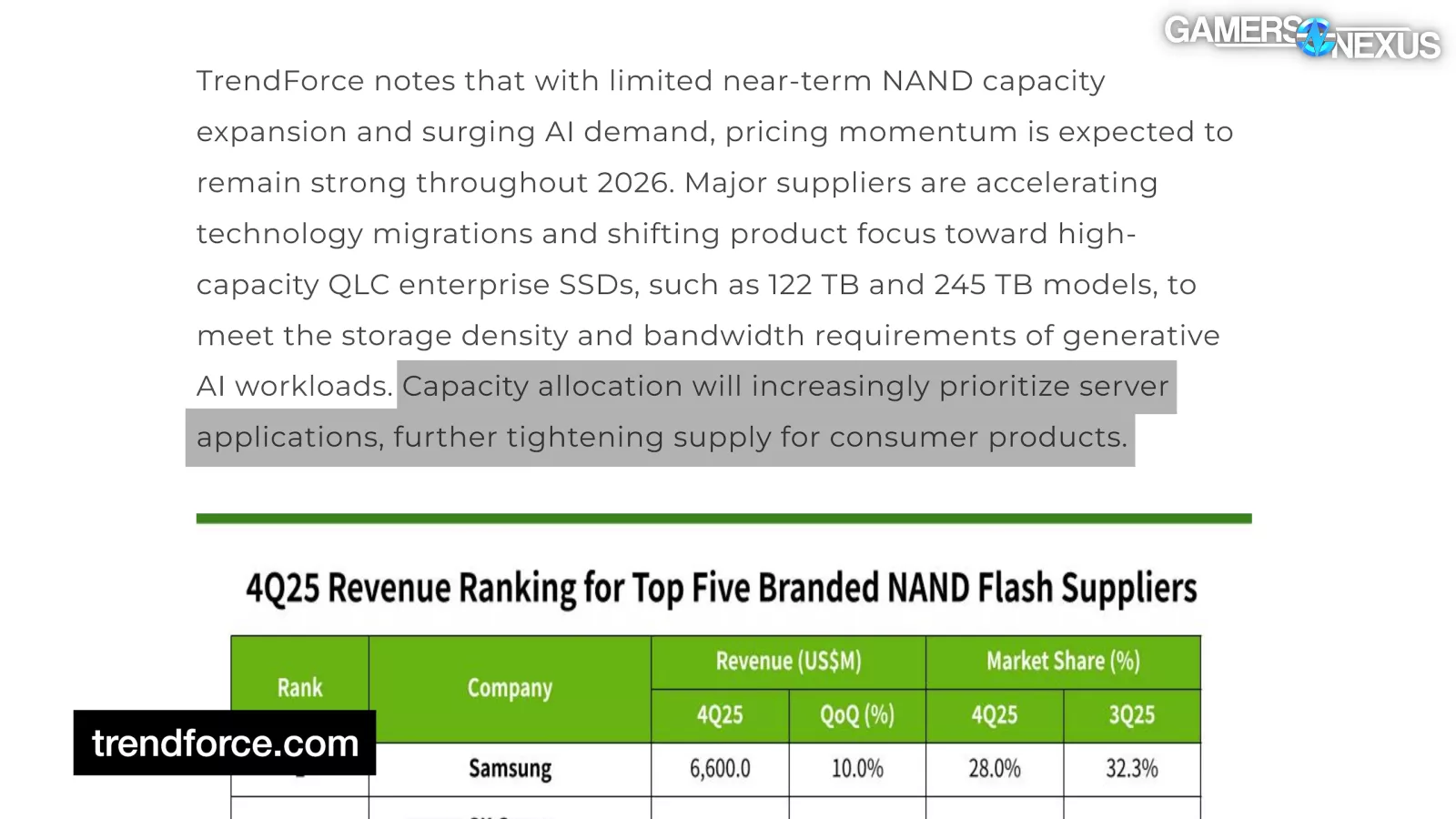

“Capacity allocation will increasingly prioritize server applications, further tightening supply for consumer products.”

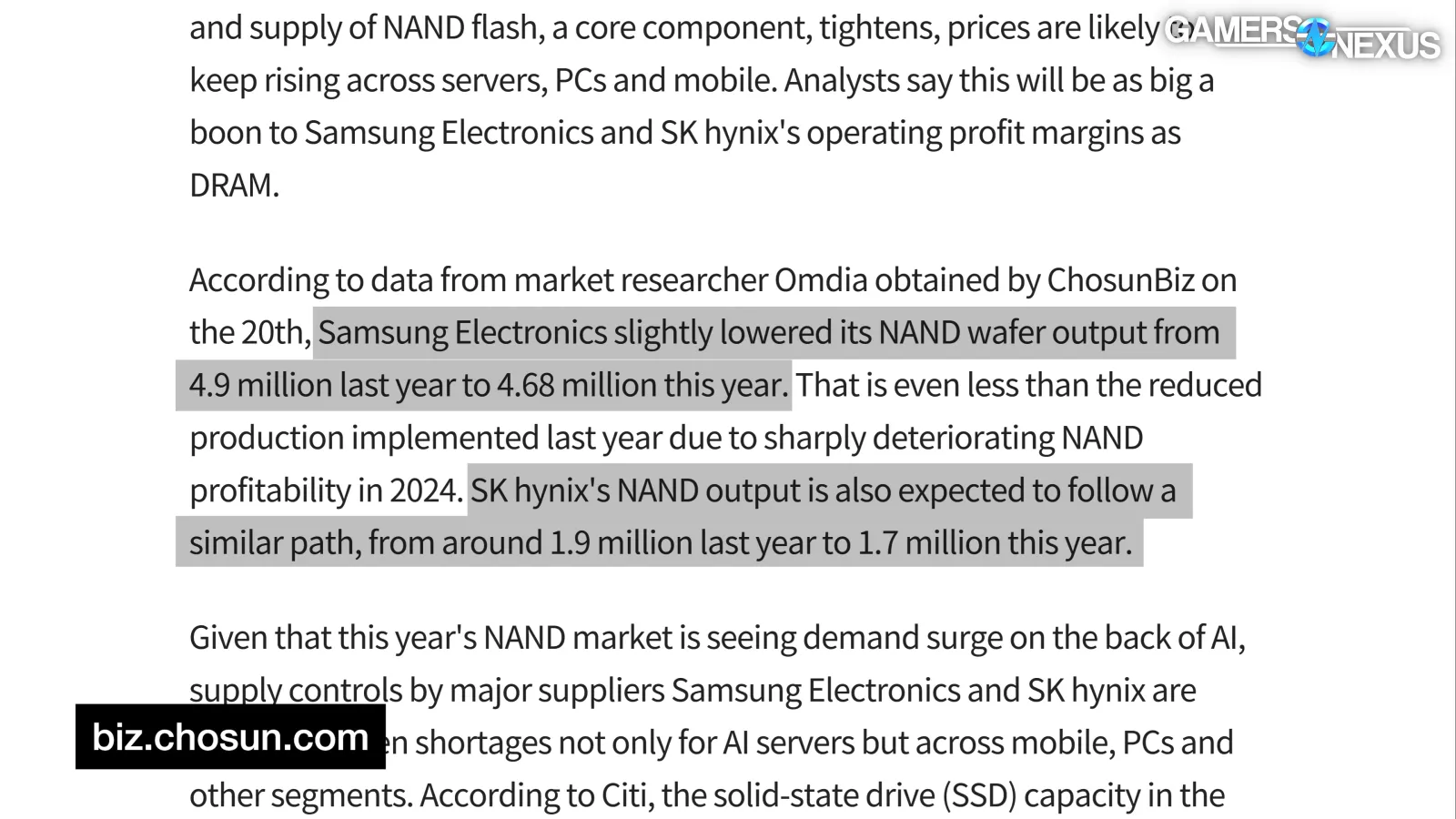

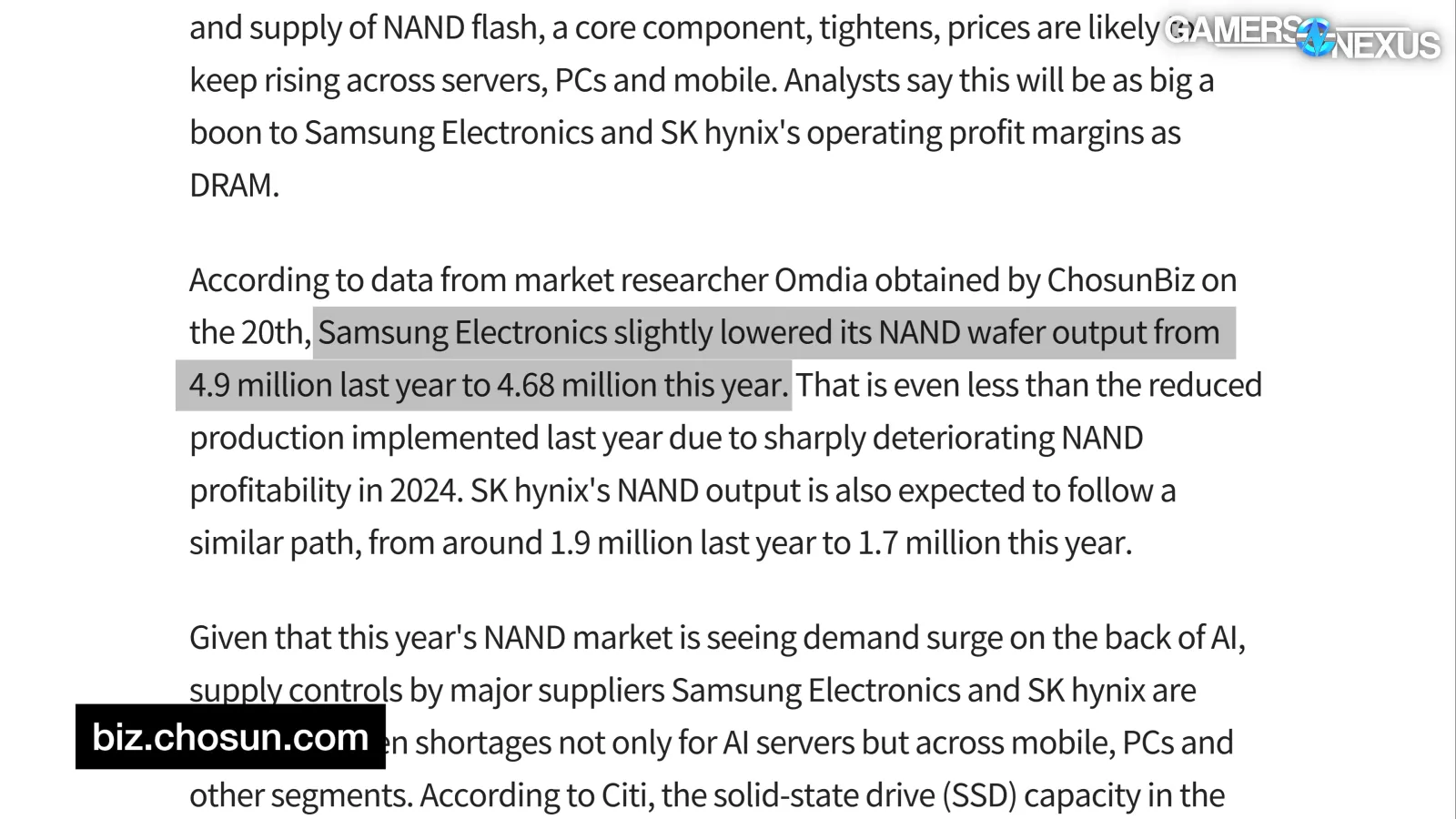

And now, at the height of the demand for NAND Flash, the manufacturers have reportedly begun cutting NAND production from its output last year, with Chosun Biz reporting (through machine translation), “According to data from market researcher Omdia obtained by ChosunBiz on the 20th, Samsung Electronics slightly lowered its NAND wafer output from 4.9 million last year to 4.68 million this year. That is even less than the reduced production implemented last year due to sharply deteriorating NAND profitability in 2024. SK Hynix's NAND output is also expected to follow a similar path, from around 1.9 million last year to 1.7 million this year.”

So at peak demand and as demand is actually growing annually, some of these companies are cutting production, and as far as we can tell, they're doing it to maintain higher prices. That sure sounds familiar…

Conclusion

Our conclusion today is simple. SSD prices are absurd, obviously, but it looks like it’ll get worse. Generally, we try not to make any predictions because it’s just us throwing darts at a board. We don’t have any more insight than you, and most of our information is from digging through earnings reports and bank reports, all of which are public.

But, to guess at it, our best guess is that completed consumer drive prices will increase rather than decrease in the near-term. If anything, there’s been a lag on price increases versus manufacturing cost increases.

To quickly recap: Due to a mixture of SSD and HDD shortages, unprecedented AI server and data center storage demand as servers transition to NVMe drives, and manufacturers with a long history of collusion choosing to cut supply further amidst the shortage: NAND Flash wafer spot prices are increasing at an even faster rate than DDR5, with 512Gb TLC Wafer’s spot price currently sitting at 8.57x its previously stable price held between July and September 2025.

Furthermore, major manufacturers are running out of capacity for 2026, like Kioxia, which already sold out of its SSDs, and Western Digital, which already sold out of its hard drives.

{kind=link}

Current DDR5 RAM kit market prices still hold a greater percent increase than SSD market prices, but we expect SSD prices to skyrocket in the near future as the consumer market eventually shifts to reflect the most recent spot market changes.

As an aside, we have some first hand experience with this. We bought over 10,000 USB flash drives at 128 GB each for our Kickstarter style campaigns we did for our black market movie. As part of the backer tiers, we sent out flash drives with some of our videos loaded on them. And we bought them from Micro Center. But right now, they can't really supply us with more because the pricing is out of whack and isn’t predictable.

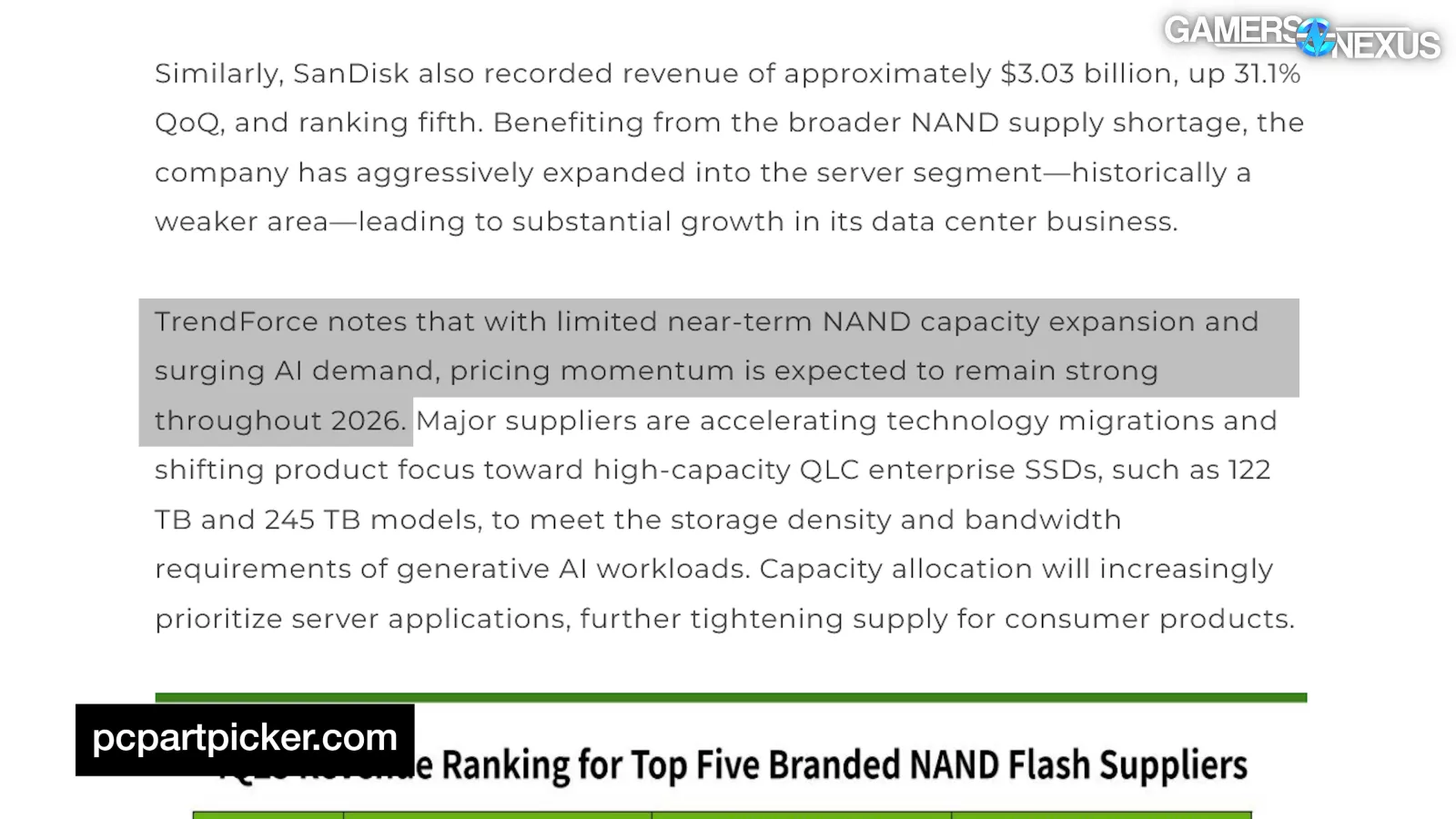

In terms of forecasts, TrendForce’s most recent NAND Flash report reads:

“TrendForce notes that with limited near-term NAND capacity expansion and surging AI demand, pricing momentum is expected to remain strong throughout 2026.”

If you’re wondering if there’s anything you can do, there’s not. If you’re wondering if there’s anything the manufacturers can do, frankly, we wouldn’t be surprised if they cut production further to raise prices even higher.

So if you’re wondering what the fuck happened to the SSD prices, then this story provides your answer (It’s the same thing that happened to the RAM prices).